Tawanda Musarurwa

Check Point Desk

For many Zimbabweans, falling ill is as much a financial crisis as it is a medical one.

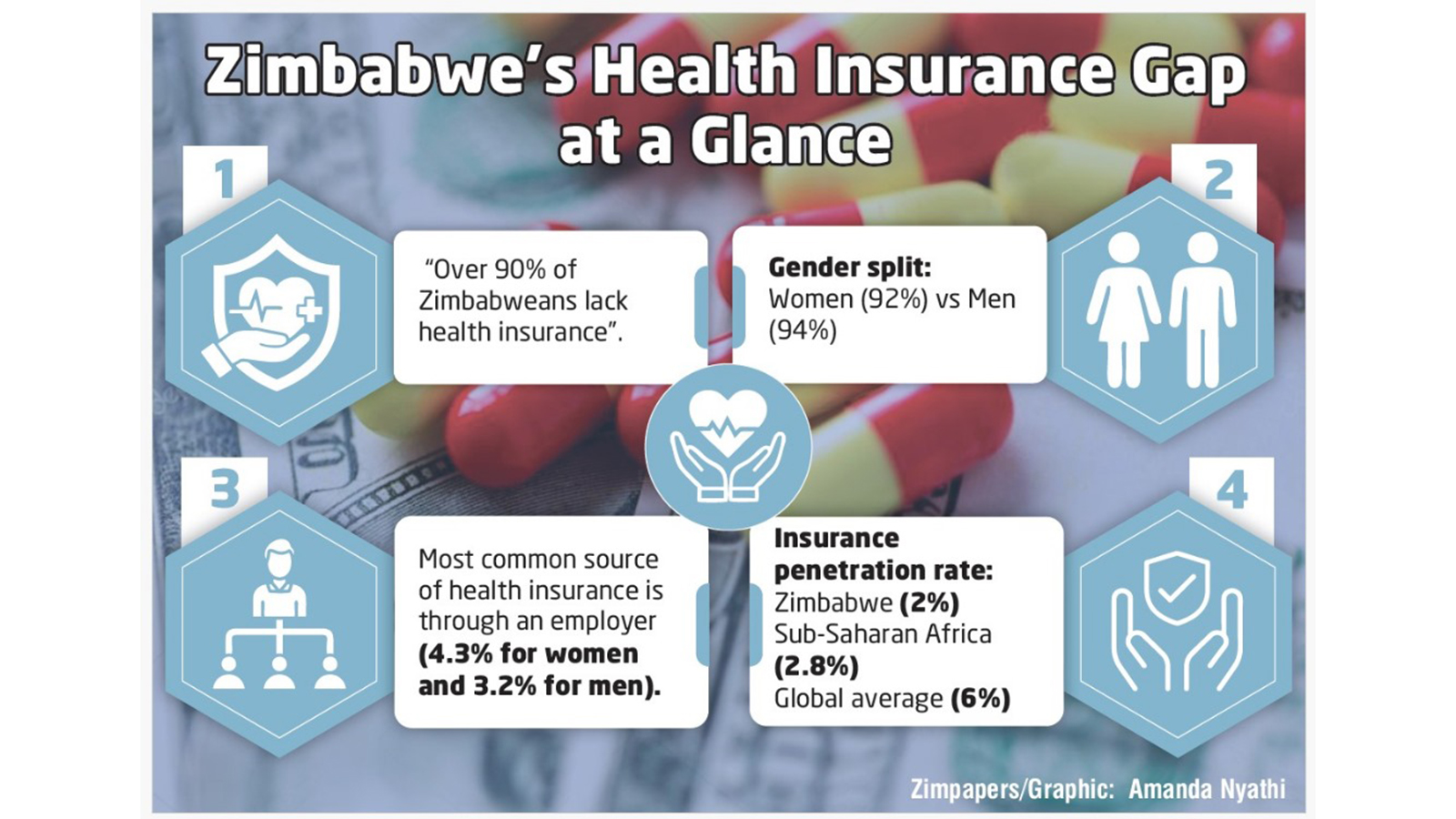

According to the 2023-2024 Zimbabwe Demographic and Health Survey, over 90 percent of adults (92 percent of women and 94 percent of men) lack health insurance.

This reflects the country’s low insurance penetration rate, which stood at just 2 percent in 2024 — below the global average of 6 percent and the Sub-Saharan Africa average of 2,8 percent.

Only a minority, mostly those in formal employment, are covered through their workplaces.

The ZDHS data shows that the most common source of health insurance is through an employer, with coverage at 4,3 percent for women and 3,2 percent for men. A decade ago, coverage was improving, but it has regressed from between 11 percent and 12 percent in 2015 to just 8 percent in 2024.

In theory, insurance pools risk by collecting premiums from many to cover the medical costs of a few, spreading expenses and protecting individuals from catastrophic out-of-pocket costs.

However, when few are insured, costs rise and premiums become harder to afford.

Families are often forced to choose between treatment and survival. For a household earning the equivalent of US$300, one hospital admission can wipe out three months’ income.

A Check Point survey found that private doctors typically charge consultation fees ranging from US$20 to US$80, depending on location and specialty.

Basic laboratory tests cost between US$30 and US$70, ultrasound scans average around US$10, and CT scans range from US$50 to over US$180, far beyond the reach of many Zimbabweans. Private hospital admissions, excluding medication, can exceed US$500.

With health costs this high, insurance is failing to act as a safety net.

The Price of Getting Sick

For many, health insurance is a promise that exists only on paper. When 37-year-old market vendor Ms Loveness Moyo’s teenage son needed an emergency appendectomy, she did not call a doctor; she called relatives and friends. Her medical aid card had expired months earlier after premiums nearly doubled overnight.

“I used to pay every month, but the price went up faster than my income,” she said. She is one of many forced to rely on out-of-pocket payments for healthcare.

Public data and industry figures confirm that private medical cover remains the preserve of a small minority.

Economic Realities Unravel a Constitutional Right

Section 76 of the country’s Constitution guarantees every citizen the right to basic healthcare and compels the State to take reasonable measures to ensure access.

In principle, this right should shield families like Ms Moyo’s from medical bankruptcy. In practice, it is constrained by affordability and weakened by policy gaps.

Health is also enshrined in Sustainable Development Goal 3 (SDG 3), which calls on nations to “ensure healthy lives and promote well-being for all at all ages.”

However, more than a decade into the SDG era, Zimbabwe’s health insurance market still serves the few.

Public health expert Professor Johannes Marisa of Great Zimbabwe University’s Simon Mazorodze School of Medical and Health Sciences expresses concern: “Indeed, less than 10 percent of our population is insured; this development is worrisome. The rate of formal unemployment is a significant factor, as many people cannot afford regular premiums charged by medical aid societies. There is also a general lack of confidence among the populace due to ongoing disputes between service providers and insurers. Even those insured often face substantial shortfalls demanded by service providers.”

“Non-payment by medical aid societies and their aggressive tactics have left many service providers with no choice but to reject medical aid cardholders. This slows the growth of the health insurance sector and pushes many to rely on out-of-pocket payments,” he said.

Chasing Margins

The Insurance and Pensions Commission (IPEC)’s Second Quarter 2025 Short-Term Insurance Sector Report paints a complex picture.

Health-related insurance remains a modest share of total short-term business, but it is one of the fastest-growing segments, expanding by 88,1 percent between June 2024 and June 2025. This surge signals a strategic shift as insurers increasingly view health coverage as a new growth frontier. IPEC attributes the renewed momentum partly to macroeconomic stability.

Following a GDP rebasing to US$45,7 billion from US$35,2 billion, the economy has become more resilient, with financial and insurance services contributing 10,8 percent to national output.

Stabilising inflation and exchange rates have also made needs-based products like health insurance more attractive.

However, the Q2 report cautions that market concentration and currency volatility remain major risks. The dominance of US dollar-denominated policies creates barriers for local-currency earners and exposes insurers to exchange-rate shocks.

The cancellation of Vivat Health Solutions’ licence in April 2025 — a subsidiary linked to Old Mutual — reflects both tighter regulation and corrections in health distribution channels.

Deep structural imbalances persist. Traditional classes such as motor and fire insurance still dominate, with motor alone accounting for nearly half of all short-term premiums, while health remains underdeveloped.

Economist Dr Albert Makochekanwa of the University of Zimbabwe Business School attributes this to both economic and behavioural factors.

“With motor insurance, there is nothing to celebrate from a company (or industry) point of view; it’s mandatory by law. Poverty means insurance is treated as secondary, including health insurance,” he said.

Building Inclusion from the Ground Up

The sector has shown potential for growth. At a broader level, the share of women with insurance increased from 7 percent in 2010–2011 to 11 percent in 2015, but dropped to 8 percent in 2023–2024, according to ZDHS data.

Similarly, men’s coverage rose from 9 percent to 12 percent over the same period before falling back to 8 percent.

At the industry level, the micro-insurance sub-sector recorded 124 049 active policies as of June 2025 — covering health, legal aid, and funeral plans — indicating deepening inclusion among low-income earners.

Regulator data shows micro-insurers wrote US$190,870 in foreign currency-denominated health insurance premiums in Q2 2025, a 74 percent year-on-year increase.

Health micro-insurance grew by 88,1 percent, driven by rising demand and better cross-selling.

Micro-insurers can extend health coverage to communities long overlooked by traditional providers, but progress remains uneven.

About 67 percent of micro-insurance is now written in foreign currency, boosting stability but widening inequality as local-currency earners are priced out.

Smaller players face compliance and liquidity pressures, despite aggregate capital rising 39,6 percent to US$5,42 million.

While most (seven out of the total of nine operational micro-insurers) now exceed the regulator’s US$100 000 minimum capital threshold, consolidation or partnerships may be needed to stay solvent.

IPEC’s Q2 2025 report indicates a shift from survival to strategic repositioning, with health insurance emerging as a key pillar of growth and inclusion.

Capital adequacy and compliance reforms could foster innovation, digital health partnerships, and micro-health insurance expansion.

Real inclusion, however, demands new incentives and business models. IPEC’s push for structural diversification into health, savings, and legal aid should be backed by flexible compliance for high-volume, low-margin products.

These emerging segments collectively outpaced the sector’s 34,7 percent growth rate, underscoring structural transformation.

Local insurers could leverage the country’s thriving mobile money ecosystem, which handles over 70 percent of national transactions, according to central bank data.

While micro-insurers are expanding access from the bottom up, universal coverage will require broader risk pooling and public-private coordination to make protection affordable and sustainable.

Widening the Pool

Government-backed pooling could spread risk and stabilise premiums. Examples such as Kenya’s National Hospital Insurance Fund and Rwanda’s Mutuelles de Santé show that even partial subsidies can unlock mass coverage.

In September, Health and Child Care Minister Dr Douglas Mombeshora stated that the draft National Health Insurance Scheme Bill has been finalised and could become law by year-end.

However, expanding coverage will test fiscal discipline and political will. Private insurers may resist subsidised competition, while healthcare providers push for higher tariffs.

The alternative is the status quo — a fragmented system where formal workers receive care and everyone else improvises.

Zimbabwe spent about 4 percent of GDP on health last year, far below the 15 percent Abuja target. Without an effective health insurance framework, the 2030 universal health coverage goal may remain out of reach.

Reform and Regulation

Even among the insured, concerns about poor service quality persist. One of the biggest issues is shortfalls and co-payments, often caused by tariff disputes between medical aid firms and service providers. However, clients’ concerns vary widely, with each raising different issues based on their unique experiences and expectations.

Forty-two-year-old Mr Simon Muza (*not his real name), who suffers from chronic allergies, says his medical aid society — one of the largest in the country — does not cover allergy medication.

“I have to pay out of pocket for my nasal spray and cetirizine tablets,” he said. “It never made sense to me. I thought medical aid was meant to protect me from high healthcare costs.”

This has prompted the regulator to act. The IPEC Amendment Bill (2024) proposes to grant IPEC authority to regulate medical aid societies. The Commission argues it is better equipped to oversee financial integrity, solvency, and governance — areas beyond the Ministry of Health and Child Care’s core mandate.

“We are still waiting for Parliament processes,” said IPEC public relations manager Mr Lloyd Gumbo.

However, the Association of Healthcare Funders of Zimbabwe (AHFoZ) questions IPEC’s capacity. “The challenges facing the healthcare sector require solutions driven by those within the sector, not imposed by external bodies unfamiliar with its complexities,” said AHFoZ chairperson Mr Stanford Sisya during a meeting in April.

Closing the Loop

Back in Mbare, Ms Moyo finally cleared her son’s hospital bill using three months of savings and a loan from her church group, which charges 10 percent monthly interest.

The operation was successful, but the debt has chained her to relentless work.

“Every dollar I now earn has already been spent twice over. I don’t know when we will be free,” she said.

Her story is a quiet verdict on the country’s health insurance system. The Constitution and the SDGs promise health for all, but a promise is not a plan.

Until the math of risk is rewritten and the architecture of exclusion dismantled, that promise will remain a price tag the majority can see, but only a few can afford.