Clifford Shambare

Inflation is a phenomenon that is dreaded by most of us; this is particularly so among the bankers and economists who are the people tasked by the (economic) system, to take care of such matters. So what is this beast called inflation? In layman’s terms inflation is any rise in prices of goods and services that can easily assume a mode of inexorability. In almost all cases, whenever inflation raises its ugly head, most of us are bamboozled by it largely because we do not know why or how or what forces trigger it.

Let us try to tease the issue here and hopefully end up understanding better, how the phenomenon works and how it is harming the Zimbabwean economy as well as how we should solve the problem.

Inflation essentially arises from the existence of too much money chasing too few goods in an economy but in practice, the situation is more complicated than this. In order to appreciate this fact better, consider that economists encourage some level of inflation in the economy, arguing that there is a level at which it stimulates economic growth — that is, not too low and not too high a level.

In order to see how this happens, one needs to recognise that there are two types of inflation; that is demand pull and cost push inflation. Although demand pull inflation stimulates economic growth, at higher levels it causes the overheating of same.

Cost push inflation on the other hand, is the trickier one of the two to manage since its source can be spontaneous; it is usually difficult to identify. And moreover, it can arise from external sources which are beyond the control of the economy concerned.

The former is the one that stimulates growth while the latter has a very detrimental effect on same, particularly if the economy concerned, depends on imported raw materials where these costs are normally determined by the exchange rate ruling at the time these raw materials are supplied. And if the economy concerned has no currency of its own — as is the case in Zimbabwe today — the situation becomes difficult to manage.

As can be expected, cost push inflation is the one form Zimbabweans are most fearful of.

As a result, most Zimbabweans and their economists are always harping on this latter form of inflation. But of course, this is an understandable position given the country’s manufacturing industry’s generally low capacity for producing tangible goods.

So in a sense, Zimbabweans are subconsciously too frightened of the challenge paused by the current circumstances, to act urgently to address the matter of production and productivity in the country’s manufacturing industries.

But this is the area in which the solutions to the country’s current economic woes are to be found.

To appreciate this fact better, when the American economy had suffered a severe contraction after the dot.com bubble and the transfer of a good part of its manufacturing industries to Asia, people like Barack Obama the then US president, solved it by resuscitating the manufacturing industry, not by trying to play around with currency exchange rates. Without this approach, his concurrent quantitative easing strategy would not have been of much help to the situation.

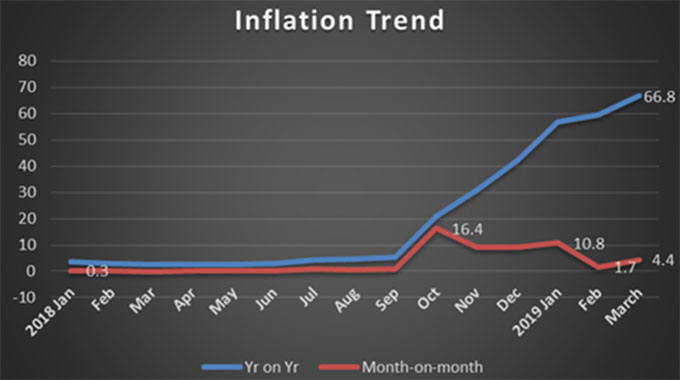

In Zimbabwe the relationship between inflation and price distortions has become a headache.

Under current circumstances the cause and effect of these two phenomena seems to be moving in either direction — that is, inflation causing price distortions and price distortions causing inflation.

In this scenario, information distortion is playing a not insignificant role despite an array of (apparently) very efficient social media.

These are circumstances in which political conspiracy cannot be ruled out even though it cannot be proven.

Although economics textbooks are awash with the subject of price distortions, the phenomenon can be quite bamboozling to the layman.

Soni explains that: “In a free market, the prices of individual commodities are set by the laws of supply and demand. An increase in demand or decrease in supply usually results in a higher price while a decrease in consumer demand or an increase in supply usually results in a lower price.

“When the price of a commodity does not follow the rules of supply and demand it is described as a cost distortion, price distortion or market distortion.”

If we look closely into the reason for the current price distortions in the Zimbabwean economy we find them to be arising from a number of sources, the most important of which is the same lack of capacity to produce tangible goods. This condition leads to a chronically low supply of those goods.

The other arises from the use of the basket of foreign currencies, in which the US dollar is the preferred currency albeit a scarce one.

Under the circumstances where the economy largely depends on imported goods from external sources, any shocks arising from the international currency exchange markets invariably enter the internal market environment almost instantly, through that channel.

In the case of Zimbabwe, if we critically examine how these two negative phenomena — that is, inflation and price distortions — have been interacting with each other, we can make some interesting observations.

In the current circumstances some reasons being given by both the manufacturers, the wholesalers and the retailers for the price increases are justified while others are not. One of them is that the raw materials used in most manufacturing processes in the country are being imported and paid for in foreign currency, mainly the US dollar.

In the case of those goods, this position could be justified but this is not the situation in all cases since there is currently, a relative abundance of products, the bulk of whose raw materials are available locally.

Incidentally, a good number of these products are in the food industry — these being maize meal, sugar, beef, chicken, beverages such as beer and mahewu, raw and tinned beans, peanut butter, potato crisps, and so forth.

And yet the prices of those goods are also rising at the same rate as those in short supply such as cooking oil, margarine, cheese, butter and fruits.

Be that as it may, let us focus our discourse on wheat flour and maize meal as examples here since these are products that most of us consume in bulk and moreover, they constitute our staple foods. The way the crop processors as represented by the millers and the bakers, are managing their industry with respect to their relationships with the suppliers — that is, the farmer and the Grain Marketing Board, and the consumer — is full of intrigue. Currently, Zimbabwe cannot produce enough wheat for her bread requirements so it has had to import the difference between local wheat production and bread consumption requirements.

Using the available figures, let us do a bit of crude costing of the bread value chain. In doing so, let us assume that all our wheat is locally produced; this approach will make our case much simpler than otherwise but this does imply that this is the actual situation on the ground.

According to US standards, one bushel — that is 60 pounds or 132 kg of wheat flour yields approximately 42 commercial loaves of white bread and approximately 60 loaves of whole wheat bread.

On converting our figures to the metric scale, this gives us 649,35 g of wheat per loaf of white bread, assuming that the weight of bran from the flour making process, is negligible.

In Zimbabwe a standard loaf of bread should weigh 700g, meaning that if this standard is the same as the American one, which it is very likely to be — about 50g of this bread is made up of other ingredients, mainly water.

This means that other things being equal, one tonne of wheat should give us approximately 1540 loaves of bread.

Before the recent price increases as set by Government, the GMB used to pay the farmer US$540 per tonne of wheat; now it pays him $1 086 00 per tonne. Surprisingly, if we convert this new price to the inaugural official exchange rate of US$1:2,5 RTGS dollars, it actually drops to US$ 434,40! If we use the black market rate — rate that has been changing fast from 3,5 to 4,2 between the beginning of April and the 16th of the same month — it drops even further, from US$ 310,29 to US$ 258,57. So, this seeming price rise is in fact, some form of devaluation of the local currency. It is moot whether the authorities knew this fact when they set the new crop prices, or it just happened by default.

At this point one can already see the major challenge to the whole Zimbabwean economy here.

The system trashes the farmer’s efforts by design or by default, and yet he/she is the base and basis of most industries in the country; the same is the case with the other crops such as tobacco and cotton. (However, let us continue with our analysis without being emotional about the issue here.)

In order to balance the equation, let us also look at the end product, bread under the new conditions. If we adjust the new price to US dollars as of the same period, we get US$1,40 per loaf. This a real increase of 140 percent on the original price of bread as compared to a fall in the price of wheat from US$540 to US$434,4 official rate and 258,57 using the black market rate as at April.

Therefore the actual rise of the price of bread accruing to the miller and the baker is 182,54 percent.

Let us now look into the changes that took place from the farmer to the bread retailer.

Under the new price regime the miller buys the wheat from the GMB at $1 086, mills it and sells it to the baker at $1 760 per tonne. Thus he puts a mark-up of $ 674 — that is 62,06 percent — on the wheat.

On the other hand, the baker bakes bread and sells to the retailer at a wholesale price we are not privy to. However, one retailer that I asked informed me that they order their bread at $3,05 a loaf. The retailer sells that bread at $3,50.

This is an income of $5 390 per tonne. So in this case the baker and the retailer share a markup of $3 630 between them — (that is 5 390 less 1 760).

However, if it is indeed the case, that the retailer is paying the baker $3,05 per loaf, then it is the baker who is getting the bulk of the mark up between the two of them while the retailer is making a gross profit of only 14,8 percent.

This level of profit is not abnormal in a retailing business where fixed costs and overheads are relatively low.

But in this case the baker’s mark-up is $ 4 697 — that is, 166,9 per tonne of flour! At this stage we do not have his production cost profile, so we cannot calculate his net profit.

However, it cannot be far-fetched to assert that some profiteering is taking place here.

Then there is the case of the mass of the loaf of bread that is being baked these days; personally, I have done some checks on the weight of an average loaf being made and sold by the established bakers and I have found that it changes in strange ways. On May 6, I weighed two loaves from Baker’s Inn and got 600 and 630g respectively; on the 12th I weighed two loaves from the same company and 700g and 702g respectively!

Let us now go to the case of maize; although there has not been as blatant as that of bread the price difference between the raw material — that is, maize grain and maize meal — is quite wide. The current price of maize that the GMB pays the farmer is $720,00 while the retail price of maize meal falls between $1 000 00 and $1 500 00 per tonne.

This case presents us with an interesting but worrying scenario. To begin with, the level of value addition on maize is quite low.

In actual fact, it needs not be complicated since the conversion of the maize seed to a meal involves the simple process of grinding or milling. So, for the simple purpose of satisfying hunger, one does not even need sophisticated packaging since a simple unlabelled grain or plastic bag is sufficient.

In such circumstances, the move to a more sophisticated presentation of the product through attractive packaging and labelling has the effect of raising the price of the final product. This in turn, has the effect of increasing the burden on the consumer who in most cases, especially in Africa — is poor.

But doing away with this part of the value chain may not be a wise thing to do since this aspect comprises another area of wealth creation and economic development.

Through such activities — which themselves, make up whole industries —many people end up being employed. In this sense Africa (Zimbabwe included) is in some sort of dilemma. (However, this part of our case should be reserved for another forum, so let us focus our discourse on the matter at hand here.)

When quizzed as to why he has raised his product price, the miller has often claimed that it is the packaging that is the culprit since it is imported and paid for in foreign currency. However, the consumer is not impressed with this argument; this is probably why people in Bulawayo — most of whom are consumers of maize meal — proposed at one point, that the Government should avail maize from the GMB, directly to them so that they could have it milled by many individual millers dotted around town. They know that the resultant quality of the maize meal is the same as that from the major millers; in actual fact, it is even better nutritionally, than its “processed” equivalent since it has all the natural components of the grain.

Embedded in these challenges is the question of subsidies that makes up its own story — a story that can constitute a whole subject of debate in the country. In this regard, interested parties have debated as to what point from which these subsidies should be effected — at the farm gate level, at the miller level, or even at the consumer level?

This is also the point at which the matter of farming input costs crops up.

The issue of corruption also crops up here. Some people in the country have claimed — not without a basis — that some individuals in high places have abused the agricultural input subsidy scheme, right across the board — from the stage of basic farming inputs through grain purchases from the GMB, to product packaging. In this respect, remember the grain bag scandal of 1987, that resulted in the sacking of the then CEO of the GMB?

Considered in their totality, these are the sort of nefarious practices that end up resulting in a typical case of food (based) inflation — a challenge that is currently dogging the whole of Africa today, in the process contributing significantly to a perpetual state of hunger on the continent.

Clifford Shambare is an agriculturist-cum-economist reachable on — 0774960937 or [email protected]