Tapiwanashe Mangwiro

The Reserve Bank of Zimbabwe (RBZ) has held its benchmark Bank Policy Rate (BPR) at 35 percent, underscoring its commitment to a tight monetary policy stance designed to anchor inflation expectations and sustain exchange-rate stability.

In its Mid-Term Policy review Statement released yesterday, the RBZ reiterated that it would stay the course of the current stance, while remaining flexible to signals informed by incoming data on inflation, the exchange rate, economic activity and other key macroeconomic fundamentals.

Governor Dr John Mushayavanhu defended the decision, pointing out that with annual inflation projected to end 2025 at around 30 percent, the existing policy rate delivers a real interest rate of 5 percent, which is consistent with the natural rate observed in other countries.

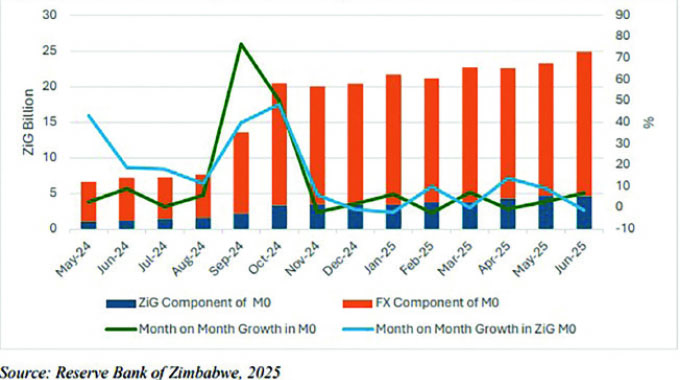

The RBZ’s “Back-to-Basics” framework continues to use reserve money control as its operational target, with the floating ZiG/US$ exchange rate serving as an intermediate nominal anchor.

“For the avoidance of doubt, the Reserve Bank is not using the exchange rate as the operational target,” Dr Mushayavanhu clarified. “We are using a market-determined floating exchange rate and only influencing its movement through ensuring prudent management of reserve money.”

This approach has underpinned a sharp slowdown in monthly inflation, which averaged 0,6 percent between February and July 2025, even as annual ZiG inflation remained elevated due to base-effect distortions.

The central bank projects that sustained low monthly inflation will drive annual inflation towards 30 percent by year-end.

While some stakeholders at consultative meetings in July urged a cut in the BPR to spur lending and investment, the Governor insisted, “Inflation has largely been a monetary phenomenon in Zimbabwe, and that premature rate reductions could rekindle volatility.” He added that the RBZ would only consider lowering rates when inflation has gone below the policy rate in order to foster the optimal level of positive real interest rates.

Banker Raymond Madziva welcomed the central bank’s caution but urged a faster pivot once disinflation gains are firmly entrenched.

“Maintaining 35 percent through the disinflation cycle has helped stabilise the market, but a gradual, data-driven easing from early 2026 would support credit growth,” Mr Madziva said.

He noted that commercial banks were sitting on sizeable liquidity buffers, and a calibrated rate cut could unlock productive sector financing without risking a resurgence in price pressures.

Alongside the policy rate decision, the RBZ maintained minimum deposit rates at 5 percent for ZiG and 2,5 percent for US dollar deposits, and held time-deposit rates at 7,5 percent and 4 percent, respectively.

The central bank also preserved the 30 percent foreign currency surrender requirement for exporters, pending the unveiling of a de-dollarisation roadmap in the forthcoming National Development Strategy II.

The RBZ has further refined its monetary toolkit by tightening Non-Negotiable Certificates of Deposit (NNCDs) to a fixed 30-day, zero-coupon tenor with no early redemption, aiming to mop up excess liquidity and reinforce its reserve-money targeting framework.

Economic analyst Amon Buhali praised the RBZ’s transparency and stakeholder engagement, but cautioned against complacency. “The Mid-Term Review reflects a maturing central bank, yet external risks, from tighter global financial conditions to potential drought impacts, call for continued vigilance,” Mr Buhali observed.

He recommended that the RBZ complement its monetary stance with clearer forward guidance, particularly around the de-dollarisation timeline, to anchor market expectations more firmly.

Governor Mushayavanhu insisted that communication would remain integral to policy effectiveness. “We have adopted communication as part of our monetary policy toolkit to shape expectations, enhance transparency and increase the effectiveness of monetary policy itself,” he added.

With domestic growth forecast to rebound to 6 percent in 2025, driven by agriculture, mining and manufacturing, the RBZ underscored that its primary objective remains price stability without undermining growth.

As the RBZ navigates the final stages of de-dollarisation and global headwinds intensify, market analysts will be watching for any signs of a policy pivot once disinflation has been firmly secured.

Despite calls for rate cuts, the central bank’s mantra remains clear: durably anchor inflation and exchange-rate stability, even if it requires staying the course at peak policy settings for longer than many had anticipated.