Wafa Kuchera and Walter Mandeya

This has been the experience of many households and businesses across the country, as they grapple with the effects of the debilitating load shedding by Zimbabwe’s sole electricity supply utility, ZESA. To cope, households have been forced to invest in alternatives such as solar, gas and firewood at great expense.

The energy situation is now a fact of daily life and there is little option but to take it on the chin and adapt. However, at policy level there is need to develop more comprehensive responses to the energy challenges and assist the more vulnerable absorb the costs of transitioning to alternatives, while the national generative capacity is being addressed.

The economics of not having energy as a utility

In one of the recent discussions on the topic of power supply challenges a comment was made that “by now everyone should be able to afford solar” because the cost of solar panels has reduced significantly.

It might be true that the cost of solar panels has reduced, but the costs to install adequately robust rooftop solar systems remain relatively high. A solar system represents a significant portion of annual income for low to medium income households and small businesses which is financed upfront in cash.

This is usually paired with gas, meaning a gas tank and accessories are required. Because of the nature of Zimbabwe’s economy, which is highly informal, these investments represent significant working capital that is put into passive depreciating assets.

This allocation of capital should be of concern to policymakers in the same way that our investment in non-commercial vehicles should be of concern. The Industry and Commerce Minister, Mangaliso Ndlovu, recently noted that we spent US$3 billion on vehicles and over US$370 million on tyre imports over the past six years.

We are taking away capital that could be used to grow small family businesses, buy productive machinery and equipment, fund large scale infrastructure, fund innovations and research and putting into a highly fragmented network of small rooftop solar installations and LPG gas outlets that do not connect back to the utilities efficiently to generate state/utility level savings.

Again, for the same reasons highlighted, the investments at household level will never be robust enough, meaning that there is always need for the alternative to be augmented by ZESA (main grid) supply, maybe firewood or coal in some cases, meaning households end up using productive daylight time “figuring” out how to manage their energy requirements.

Spending time on activities that should be provided at utility level across the economy is one of the reasons why we have lower national productivity overall. We are effectively duplicating efforts across the economy in ways that do not harness any productive or value added outputs.

Electricity supply situation

The ZESA executive chairperson gave a briefing on the electricity supply situation during a recent Zimbabwe-Zambia (Zim-Zam) Energy Projects Summit that included an outline of initiatives to end load shedding by December 2025.

He provided the breakdown below which has coal fired stations providing the bulk of the new supply at about 55 percent, solar providing about 30 percent, battery storage at 15 percent and the balance of 100MW coming from wind to be situated in Mamina in the Mhondoro District of Mashonaland West.

What is interesting from the projects expected to come online in 2025 is that the majority of the new capacity will be delivered within 12 months of ground breaking.

This is testament that the new technologies being installed can resolve our power challenges as rapidly as the projects can be pre-approved and funded. In fact, ZESA presented their plan to provide universal access to electricity to an additional two million households by 2030 through a combination of grid connections, rooftop solar systems and microgrids.

This confirms that treating rooftop solar systems as a utility level service is definitely something the policymakers need to consider to be able to realise the efficiencies of scale and create financial savings that can be deployed more productively elsewhere within the economy.

From generation to distribution

By 2030 over 1 600 kilometres of transmission will be laid along 13 routes at a total cost of US$787 million (giving about US$489 732,42 per kilometre). Such an expansion of the already extensive national grid in the envisioned timeframe is ambitious. The economic benefits to be harvested along the 13 routes will be transformative.

That is the economic benefits from the infrastructure works, but more crucially, the benefits that accrue when new businesses and communities connect to a reliable power source and are able to fully participate in not only the national economy, but also in the global economy through access to the internet, for example.

It is for this reasons that it is necessary for ZESA to continue providing such briefings on a regular basis to calm nerves on the one hand and provide their customers with some basis on which to plan their investments well in advance so as to be able to mobilise resources and avoid wastage of opportunities and capital.

Zesa’s need for new structures

Alongside the ambitious plans to end load shedding by December 2025 and laying over 1 600 kilometres of transmission cables into new areas, ZESA has had to welcome new shareholders, The Mutapa Investment Fund.

The entire shareholding in ZESA Holdings and all subsidiaries was transferred from central government and vested to The Mutapa Investment Fund through Statutory Instrument S.I. 156 of 2023 and subsequent instruments.

This was definitely a positive development, for ZESA in particular, as The Mutapa Investment Fund will have greater institutional capacity to support ZESA’s ambitions with more innovative funding models, less red tape and generally more commercially oriented initiatives.

It is not clear how much credit should be given to the change in ownership, but ZESA has definitely become more communicative over the past year.

They have given a couple of detailed public statements on the state of affairs within ZESA and now the Summit presentation has given a clearer glimpse into the plans being implemented and the challenges being faced by the organisation.

Clearly, the situation at ZESA is complex as it needs to deal with inadequate funding, infrastructure that has seen better days, a shift in generative mix from mostly hydro and coal to now include renewables like solar and wind.

Finding an accommodation with Independent Power Producers (IPPs) and equity/venture partners under the Public Private Partnerships (PPPs) who now have a greater say in parts of ZESAs operations.

Major changes to some core systems for example to the billing system with the introduction of net metering and it’s nuances.

And a tariff that is exposed to serious currency risks while operating in a multi-currency environment that makes it difficult to fully recover costs, which are exacerbated by a reliance on energy imports from regional power producers.

Added to the above, Government took a policy position to re-consolidate ZESA by merging back subsidiaries that had previously been demerged in the early 2000s. From outside looking in, there is need for some changes in how ZESA is organised to make it better suited to handle the headwinds it faces.

No doubt, The Mutapa Investment Fund team, together with ZESA executive and management teams, would be ceased with this point of concern. Key ,however, is ensuring that the human capital base is progressively better resourced to retain and enhance skills which have been leaking from the organisation.

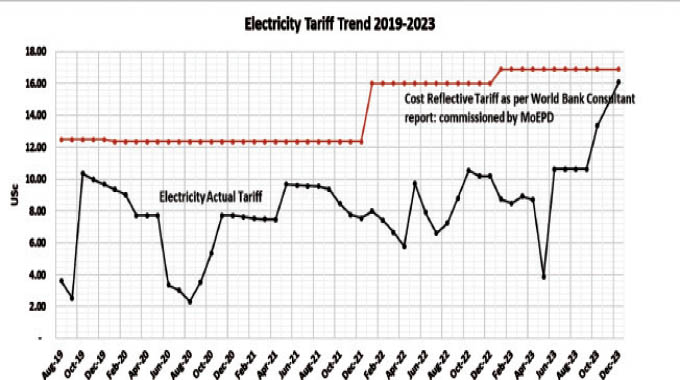

The Cost Reflective Tariff Conundrum

Top of the challenges facing our energy sector is the level of tariffs they are allowed to charge coupled with the currency they are allowed to use. Starting with the currency, Zesa is allowed to negotiate with their larger customers for them to pay in USD with the rest charged in the local ZiG (ZWG) currency.

Domestic customers are, however, free to pay in either ZiG or USD and also negotiate with ZESA if they want to pay exclusively in USD. ZESA also has to negotiate with Independent Power Producers (IPPs) and equity/venture partners under the Public Private Partnerships (PPPs) for a USD price to receive their energy into the national grid.

Coming back to the tariffs. ZESA was given approval to charge a “cost reflective tariff in December 2023” by the Government. That means ZESA is now charging a tariff that reflects their cost to generate a unit of electricity.

The tariff is set in USD and tracks the daily official exchange rate to give a ZiG tariff at the point of payment. Prior to December 2023, ZESA’s tariff was set at a certain level for a period of time after which it would be reviewed and a new tariff set.

The supply of electricity below the cost of generating it served as a way for Government to support the wider economy, but the tradeoff was under investment in skills, generative capacity and infrastructure maintenance by zesa.

This situation unfortunately dates back much longer than shown in the graph, meaning the country is possibly decades behind in terms of being able to provide itself with the energy needed to simply keep up with other nations, let alone to exceed them.

Our only hope now is that we can leapfrog straight to the latest technologies that give us much better output efficiencies. In the earlier table above, coal-fired stations take much longer to deliver compared to solar and wind installations of the same output capacity, barring the technical baseload challenges. But these utility level technologies are not cheap.

However, the country could meet its generation targets ahead of 2030 if the tradeoffs are understood and accepted by the wider public who will have to foot higher bills, until generative capacity allows for net energy exports.

And here lies the conundrum. As an observer, plugging the energy generation gap by increasing generative capacity with the tradeoff that customers pay more (for a while) seems to be the sensible solution.

However, as a customer, being made to pay more to correct ZESA and government’s under investments would be a bitter pill to swallow. As a customer, paying the current “cost reflective tariff” is understandable, but not paying more than that.

Accepting to charge or pay a higher tariff would be problematic for both ZESA and it’s customers respectively in that context. The currency issue adds to this conundrum, but also holds the solution.

Whatever higher (or normal) tariff gets charged guarantees higher tariffs in future because the tariff will never cover for the inevitable economic losses incurred between collecting a local currency tariff to meet forex related expenses incurred to generate the power. The gap between tariff revenue and costs of generation remains negative unless a solution is “agreed” to mitigate the currency risks faced by ZESA.

How can this impasse be resolved? ZESA executives clearly have their work cut out for them. They are obviously ceased with these issues on all fronts as demonstrated during the Zimbabwe-Zambia (Zim-Zam) Energy Projects Summit.

But unless people can flip a switch and get that electricity flowing into their homes and businesses, it is going to be difficult to convince the general public of their sincerity in the face of 18-hour power cuts. The only suggestion we can make towards this effort is that Zimbabweans when informed and educated about matters affecting them, they tend to respond positively to that engagement.

To other matters Zesa

ZESA is a massive countrywide operation tasked with the generation and distribution of electricity across the country. They operate with over 500 hundred highly skilled employees stationed across the country who deal with highly technical engineering challenges.

They also deal with serious vandalism to infrastructure, outright theft, losses due to weather events, accidents and much more just to keep the electrical infrastructure operational and it is amassing how they have managed on the resources they had available from sub-economic tariffs.

People are fond of reclassifying companies between categories, for example fast food chain McDonalds is said to be in the real estate business because of all the properties they own.

Fast beverages chain Starbucks is said to be a bank because of all the cash they carry on their loyalty cards.

Well, ZESA is indeed a bank because of all the cash they handle directly through their “banking halls”, through their agents and through their accounts on a daily basis. This institution is only limited by its own challenges (compounded by the previously discussed currency peculiarities) from being a true financial juggernaut.

Consider that a significant and growing number of their over 800,000 customers are on prepaid metering, meaning the customers are buying their token units a month or more in advance, providing ZESA with a cashflow boost weeks in advance of delivery of the electricity.

That ZESA is selling round-about 10,000GWh of electricity annually, which is set to increase as generation challenges are resolved.

That soon they will be capturing a good amount of passively generated rooftop solar through net-metering in addition to the over 700MWh generation anticipated to come online in 2025 from Independent Power Producers (IPPs) for onward selling.

Considering all this and the fact that ZESA still needs to connect millions of homes and businesses to the national grid to achieve 100 percent electrification, there is no reason why ZESA should be struggling with sourcing funding for new more substantial projects that provide stability to the baseload supply.

“Zesa as a bank” concept

Unlike with the technical engineering challenges that we have only observed and commented on above, we are able to actually make suggestions on the financial management of ZESAs massive cash balances held as token units in prepaid meters across the country.

Our “zesa as a bank” concept was born from our concerns on how the “gold backed” ZiG currency operates and the suggestion we made in previous articles that the ZiG should perhaps also be backed by our actual energy production as a better measure of our national productivity.

As zesa and the topical 18-hour load shedding, which we will now call blackouts, raged, we decided to shift from our annual budget prediction exercises (betting pools) to take a closer look at the country’s energy sector, focusing specifically on zesa.

We will continue our exploration of the proposed concept early in 2025 as we are taking a formal break this December.

We will try to formally and informally engage with zesa to deepen our understanding of their operations and finances as we refine our thinking around how our energy supply can support our currency and vice versa. As always, your feedback and suggestions to the email address below are always welcome.

(Written over several days from multiple locations that had electricity at the time)

(For Trigrams Investments — [email protected])