Tawanda Musarurwa

CHECK POINT DESK

NEARLY half of Zimbabwe’s pension funds are inactive, a figure that may seem alarming at first glance, but a look at South Africa tells a very different story, where four out of five funds are in the process of disappearing.

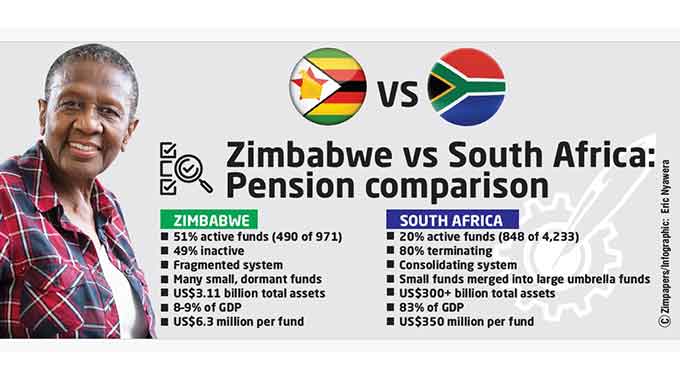

Looking at the numbers, Zimbabwe’s pensions regulator, the Insurance and Pensions Commission (IPEC), reports that as of December 31, 2025, the country had 971 occupational pension funds, with 490 active and 481 inactive — an almost even split of 51 percent active and 49 percent inactive.

In South Africa, the picture looks far more extreme. Data from the Financial Sector Conduct Authority (FSCA) shows that out of 4 233 funds, only 848 are active, while 3 385 are classified as “terminating”.

That translates to just 20 percent active and 80 percent in wind-down state.

On the surface, Zimbabwe appears stronger, with 31 percentage points more active funds. But that impression can be misleading.

When fewer funds mean a stronger system

South Africa’s pension landscape has been deliberately reshaped over the past two decades.

In her presentation at the Insurance and Pensions Symposium in Victoria Falls on Thursday, FCSA deputy commissioner Ms Astrid Ludin said the high number of “terminating” funds reflects an ongoing process of consolidation, as smaller funds are merged into larger umbrella structures.

In other words, the system is shrinking in number, but growing in scale.

“We have also very large commercial funds. That is part of the process of, over the last 20 years or so, maybe 30 years, this move from defined benefit (DB) to defined contribution (DC) has also resulted in the establishment of large umbrella funds,” she said.

On the other hand, Zimbabwe has not yet undergone a comparable restructuring.

Its inactive funds are often dormant rather than formally wound up, lingering within the system without being absorbed or resolved.

This difference becomes clearer when the data is viewed not as a count of funds, but as a measure of economic weight.

Pensions versus GDP

Zimbabwe’s pension sector holds US$3,11 billion in total assets, according to IPEC’s Pensions Report for the 12 months to December 31, 2025.

Spread across 490 active funds, that equates to roughly US$6,3 million per fund.

Set against a national economy estimated at around US$35 billion to US$40 billion, pension assets account for just 8 to 9 percent of gross domestic product (GDP).

South Africa operates on a completely different scale. The FSCA reports total pension assets of R5,84 trillion, equivalent to more than US$300 billion.

That is roughly 83 percent of GDP — a level typical of more mature retirement systems.

With 848 active funds, the average South African pension fund holds well over US$350 million in assets.

The contrast is not subtle.

Zimbabwe has more funds relative to its economic size, but each one is small.

South Africa has fewer funds, but each is significantly larger and better capitalised.

This is the dividing line between fragmentation and scale.

Quiet signals of stress

While weaknesses in the local pension system show up in the number of funds, they also appear in the flows of money and membership beneath the surface.

Starting with participation, membership in occupational pension funds fell by 15 percent to 998 072 in 2025.

While part of this decline reflects the transfer of unclaimed benefits to the Guardian Fund, it also highlights deeper issues in tracking and retaining members.

One of those issues is unclaimed benefits.

More than 104 000 accounts fall into this category (pension entitlements that have not been paid out to beneficiaries).

Then there is the problem of contributions.

According to the latest IPEC data, arrears rose by 26 percent to US$126 million, pointing to growing non-compliance among employers.

Contributions are the lifeblood of pension systems; when they falter, everything downstream is affected.

Investment patterns add another layer of risk. Around 82 percent of pension assets are concentrated in property, equities and pooled investments.

While these are standard asset classes, the concentration limits diversification and exposes funds to market volatility.

Regulatory targets are also being missed.

Pension funds are required to allocate at least 20 percent of assets to prescribed investments, typically aimed at supporting national development. In practice, compliance stands at just 8 percent.

Costs, meanwhile, are eroding value.

Pension administrators collectively recorded losses exceeding US$600 million in local currency terms, driven largely by operational expenses such as salaries and management fees.

The figures show patterns of a system that is fragmented, underfunded and inefficient.

In response, IPEC is implementing wide-ranging pension reforms focused on strengthening governance, tightening reporting standards and enhancing regulatory oversight, including new guidelines on preservation funds, revised reporting requirements and a strengthened market conduct framework.

The regulator is also driving digital transformation, reinforcing cybersecurity compliance and promoting greater investment diversification — particularly into offshore and prescribed assets — to improve transparency, operational efficiency and the long-term sustainability of local pension funds.

South Africa’s long reform arc

Ms Ludin said South Africa’s pension sector has confronted many of these same issues, but at a larger scale.

In the early 2000s, the system was characterised by high costs, weak governance, low preservation rates and fragmented fund structures.

The response has been incremental, but far-reaching. Governance reforms have tightened fiduciary standards, improved disclosure and introduced mandatory training for trustees.

These measures aim to ensure that those managing pension funds are both competent and accountable.

Preservation has been another focus.

Policies now encourage or require that retirement savings remain invested until retirement, including mandatory annuitisation of a significant portion of benefits.

South Africa is also implementing the two-pot pension system, which splits retirement savings into one portion a member can access early for emergencies and another that is preserved until retirement.

“The two-pot system is the most significant reform in decades. It has been very useful,” said Ms Ludin.

The design addresses a persistent behavioural challenge — members withdrawing savings prematurely — without removing flexibility entirely.

The country is also grappling with its own legacy issues.

Unclaimed benefits have accumulated to about R88 billion, prompting efforts to centralise records and improve beneficiary tracing.

And underpinning all of this is consolidation: the steady reduction of thousands of small funds into a smaller number of large, efficient ones.

The comparison between Zimbabwe and South Africa can be easily framed in terms of how many funds are active or inactive.

But the more revealing question is what those categories mean.

In Zimbabwe, inactivity often signals dormancy without resolution, with many funds remaining on the books, neither functioning effectively nor formally closed.

In South Africa, inactivity increasingly reflects transition.

Funds are being wound down as part of a broader effort to strengthen the system.

This is why Zimbabwe’s higher share of active funds may be pointing to the absence of consolidation.

Outcomes are the real metric

Pension systems are ultimately judged by what they deliver: stable savings, efficient investment and reliable income in retirement.

This is encapsulated in one quote by actuary and World Bank consultant Mr Rob Rusconi.

“Success is measured in prosperous pensioners,” he said.

On that measure, scale matters.

Observers say a system dominated by small funds struggles to spread costs, diversify investments or enforce governance standards.

A system built on larger pools of capital has more room to absorb shocks and generate returns.

The data shows that Zimbabwe is still operating on the first model, while South Africa is moving towards the second.

What the comparison reveals

Zimbabwe’s pension sector is not defined by a shortage of funds, but by an excess of small, fragmented ones.

The figures — 971 total funds, US$3,11 billion in assets and less than 10 percent of GDP — tell the story of a system that is wide but shallow.

South Africa’s figures — fewer active funds, but assets equal to more than 80 percent of GDP — show greater depth, consolidation and ongoing reform.

While the two economies differ in size, structure and history, the direction of travel is clear.

A robust pension system is not built by keeping funds alive. It is built by making them large enough, efficient enough and well-governed enough to matter.

“Ultimately, retirement savings management is about nothing else other than ensuring that we put as much of a member’s contributions into their ‘savings pot’ as possible,” says actuary Mr Gandy Gandidzanwa.

“Any leaks out of that pot, or in the conduits that lead to that pot, need to be plugged tightly. The larger a retirement fund is, the higher are the benefits from economies of scale that trickle down to members.”