Darlington Musarurwa recently in CHANGSHA, China

CHINA’s relentless and determined push towards a green future is evident on its roads.

Forget about the well-manicured road verges — it, too, a sign of conscious and deliberate environmental stewardship — here an increasing number of cars on the roads are electric. In fact, the International Energy Agency estimates that one in every 10 cars in China is electric.

As in other parts of the world, the new energy vehicles (NEVs) have bright green number plates, or green tags, while conventional petrol- or diesel-powered vehicles bear blue number plates.

While the green licence plates began to be implemented in cities such as Shanghai, Jinan, Wuxi, Nanjing and Shenzhen on December 1, 2016, their progressive rollout throughout the country was announced in November the following year.

The exponential growth and use of zero-emission electric vehicles (EVs) — in line with China’s ambitious and lofty goal of peaking carbon dioxide emissions by 2030 and achieving carbon neutrality by 2060 — represents a marked turnaround for a country that, as the world’s manufacturing superpower, was considered the world’s largest emitter of pollutants.

This revolution, however, was long in the making, beginning with the launch of its new energy vehicle — the YuanWang — in 1995, which marked the Asian giant’s tentative steps in the industry.

Beijing’s 14th Five-Year Plan (2021-2025) further added impetus to the new thrust.

The Centre for Strategic International Studies, a United States think tank, believes China shelled out more than US$231 billion developing its EV industry in the 14-year period through 2023.

New energy vehicle ownership in China has unsurprisingly soared to 31,4 million in 2024, up from 4,92 million in 2020, as a result.

Dominant

Over the past two decades, the industry has evolved at a breakneck pace that has made China a dominant force in the industry.

Last year, the country produced more than 60 percent of the world’s electric cars, as well as a staggering 80 percent of the batteries that power them.

Also, China’s BYD (Build Your Dreams) — a company that initially produced smartphone batteries — now leads the global EV market, having overtaken US competitor Tesla earlier this year.

By some accounts, the Asian giant now has more than 147 electric car manufacturers.

“When it comes to EVs, China is 10 years ahead and 10 times better than any other country,” Michael Dunne, an auto sector analyst, recently told the BBC.

And driven by the motivation to dominate technologies of the future, Chinese engineers continue to push the frontiers of the industry.

For example, on March 17 this year, the Shenzhen-based BYD unveiled a new charging system — the Super E Platform — that is able to charge its latest models in under five minutes.

This is naturally likely to enhance both the take-up and appeal of EVs.

Foraging for lithium

Clearly, lithium — a critical component in the manufacture of batteries for EVs — has been a game-changer.

And today, China, as the world’s largest lithium processor, has a stranglehold on the entire value chain, especially in processing and manufacturing.

Its influence, made possible by strategic investments and well-developed infrastructure for processing and manufacturing, extends from producing raw materials to manufacturing the final battery cells.

Its tentacles have also naturally spread to Zimbabwe, which boasts the largest reserves of the mineral in Africa and the fifth largest globally.

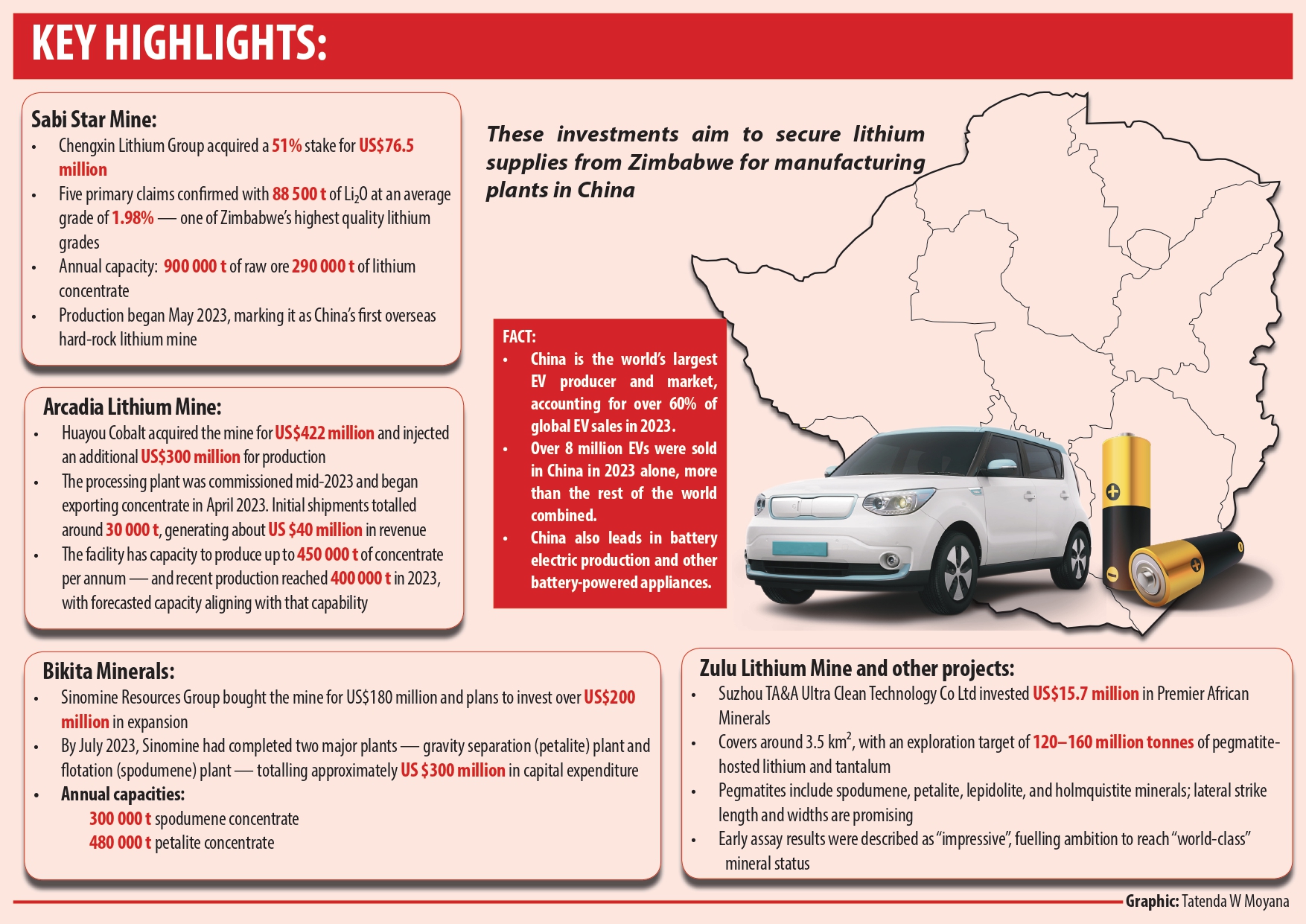

Over the five-month period from November 2021 to April 2022, Chinese investors swooped on four key local lithium assets — Sabi Star Mine, Arcadia Lithium Mine, Bikita Minerals and Zulu Lithium Mine — and spent close to US$700 million in acquisitions.

They also earmarked US$630 million for their respective expansion projects. For instance, in November 2021, Chengxin Lithium Group announced the acquisition of a 51 percent stake in MaxMind Hong Kong by its subsidiary, Shengyi International, for US$76,5 million.

This ultimately gave it control of Sabi Star Mine in Buhera, Manicaland province.

Barely a month later, on December 22, 2021, China’s Huayou Cobalt, the world’s biggest producer of the mineral, announced the acquisition of Arcadia for US$422 million.

It further injected US$300 million to expeditiously bring the project to production.

Two months later, Sinomine Resources Group (or China Mineral Resources) bought Bikita Minerals for US$180 million and announced plans to invest more than US$200 million to build a plant and expand existing operations.

Then in March 2022, Shenzhen Stock Exchange-listed Suzhou TA&A Ultra Clean Technology Co Ltd bought shares worth about US$15,7 million from Premier African Minerals in Matabeleland North.

Most importantly, the firm held a 75 percent holding in lithium hydroxide producer Yibin Tianyi Lithium Industry Co Ltd, as well as China’s largest EV battery manufacturer Contemporary Amperex Technology.

Also in Matabeleland North province, Bravura and Chinese-owned Kamativi Mining Company have invested in separate lithium projects.

Overall, all these investments were meant to lock in lithium supplies from Zimbabwe and help secure raw materials for manufacturing plants in China.

Step up

Zimbabwe is, however, not only content with being a lithium producer but wants to be an active player in the manufacture of semi-finished and finished lithium products such as glass, ceramics and, most importantly, lithium-ion batteries for both EVs and solar projects.

The Government is concerned that within the context of the ongoing global green revolution, Zimbabwe is limited to a supplier of relatively low-value raw materials.

While lithium ore is currently selling for around US$500 per tonne on the international market, battery grade lithium concentrate is averaging close to US$8 000 for the same quantity.

On June 10 this year, the Government announced a ban on export of lithium concentrates from 2027 as it pushes for local processing.

“Pertaining to the lithium sub-sector, Zimbabwe produces mainly spodumene ores, which are critical in the new energy drive. Zimbabwe’s lithium ore bodies are multi-element as they contain a number of minerals,” said Information, Publicity and Broadcasting Services Minister Dr Jenfan Muswere during a post-Cabinet meeting on June 10.

“Bikita Minerals and Arcadia Lithium are in the process of establishing lithium sulphate value addition facilities in order to beneficiate the lithium ores produced locally. With effect from January 2027, the export of lithium concentrate will no longer be allowed.”

There are promising nascent projects, such as the US$13 billion mine-to-energy industrial park, which will include the construction of two 300-megawatt power stations, a coking plant, lithium salt plant, graphite processing plant and nickel chromium alloy smelter, as well as a nickel sulphate plant.

Verify Engineering, a wholly owned Government private company, has also since made a major breakthrough in lithium battery production.

But Zimbabwe needs to step up by coming up with a robust and integrated plan for value addition of the mineral, which also includes battery production, manufacture of electric vehicles and related infrastructure. This can be encapsulated in the country’s next five-year economic plan, the National Development Strategy 2.

Without such a plan, Zimbabwe risks being relegated to a consumer. It has the resources it needs to achieve its ultimate objective — to become a modern, prosperous and highly industrial country.