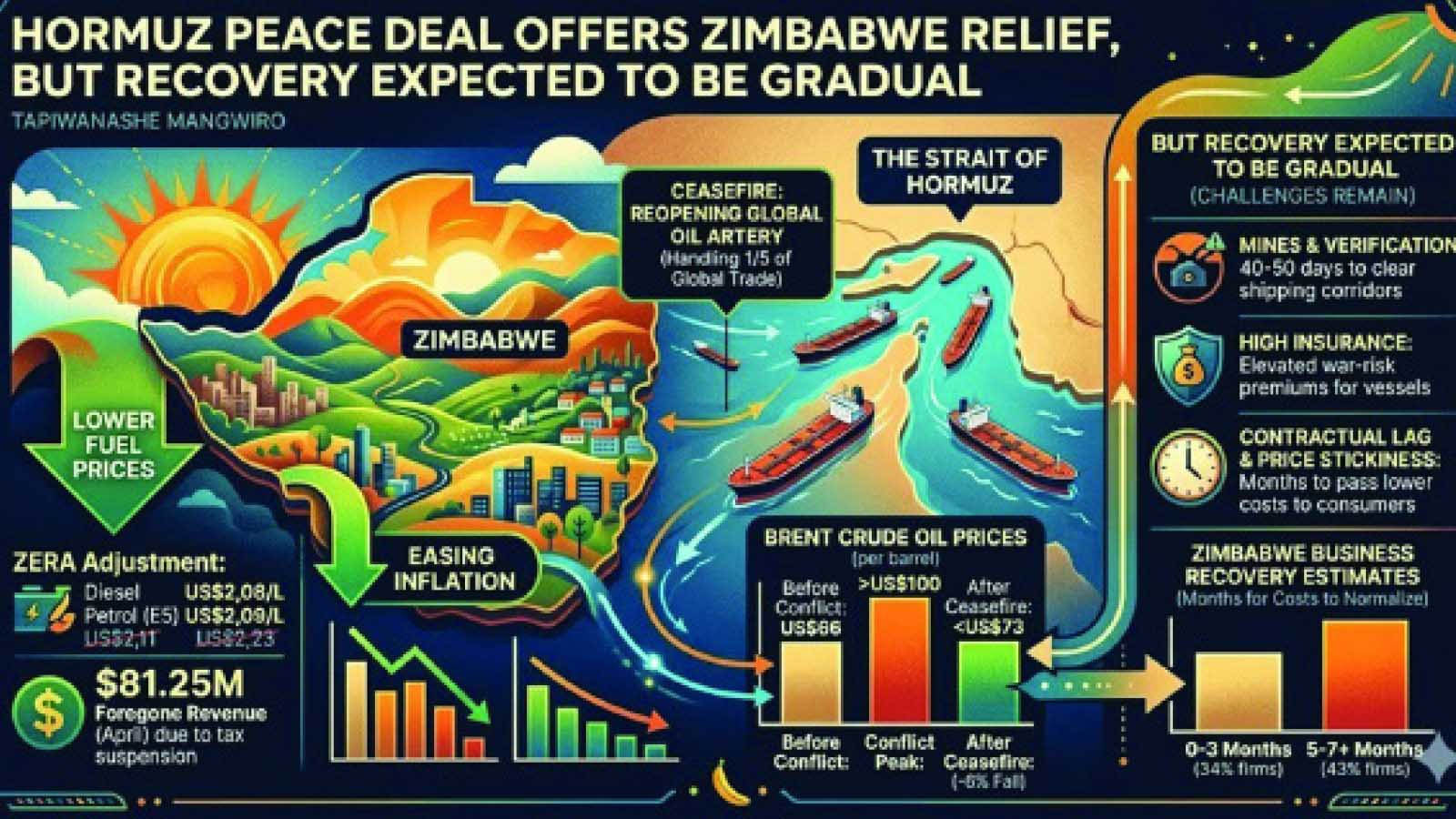

THE spectre of global supply chain disruption has once again raised its head, this time in one of the world’s most strategically vital waterways.

As Professor Nima Shokri and Dr Salome Shokri-Kuehni warn in their recent incisive analysis, which we publish this week, the potential closure of the Strait of Hormuz threatens not merely an energy crisis but also a fertiliser shock of global proportions.

For Zimbabwe, this analysis should serve as an urgent clarion call to accelerate plans already on the drawing board — those outlined in the Local Content Policy and encapsulated in the National Development Strategy 2 — to revive domestic fertiliser manufacturing capacity.

The numbers are stark and demand attention. Approximately one-third of globally traded urea passes through the Strait of Hormuz.

The Persian Gulf region, blessed with some of the world’s cheapest natural gas, has become the epicentre of nitrogen fertiliser production. Countries including Qatar, Saudi Arabia and the United Arab Emirates have invested billions in ammonia and urea capacity designed explicitly for export markets.

Any sustained disruption to shipping through this narrow chokepoint would not merely delay shipments; it would fundamentally alter the economics of global food production.

Modern agriculture, as the academics rightly observe, runs not only on sunlight and soil but also on natural gas.

The Haber-Bosch process, that century-old German innovation, remains the cornerstone of civilisation’s ability to feed itself.

Through this process, methane transforms into ammonia, and ammonia into the nitrogen fertilisers that enable wheat, maize and rice to achieve the yields on which billions depend. Without it, harvests would fall dramatically.

The world could feed only a fraction of its current population.

For Zimbabwe, this is not an abstract academic exercise. The country has recent, painful experience of how distant geopolitical events can disrupt access to critical agricultural inputs.

When the Russia-Ukraine conflict erupted, global fertiliser supply chains convulsed.

Prices soared, availability plummeted and farmers across Zimbabwe faced impossible choices: pay sharply higher prices, reduce application rates or alter crop mixes.

Each option carried consequences for national food security and the broader economy.

That experience vindicates, with uncomfortable clarity, the push to revitalise local value chains that has been central to Zimbabwe’s economic planning.

The Local Content Policy, embedded within the National Development Strategy, envisions a future where Zimbabwe reduces its vulnerability to external shocks by building domestic capacity across strategic sectors.

Agriculture, the backbone of the economy and the bedrock of food security, sits at the heart of this vision.

Yet the fertiliser component of that strategy cannot remain an aspiration; it must become an urgent priority.

For Zimbabwe, the lesson is clear: Relying on global markets for such a strategically critical input is not a strategy but a gamble.

The country’s agriculture sector, still rebuilding after years of underperformance, cannot afford to have its progress held hostage to events unfolding thousands of kilometres away in the Persian Gulf.

Unlike oil price increases, which register at the pump overnight, fertiliser scarcity reveals itself months later, when crop yields fall short of expectations.

Zimbabwe’s agriculture sector has demonstrated remarkable resilience and growth in recent years. The horticulture revival, with exports soaring past US$120 million annually, shows what is possible when conditions align.

But this success story rests on a foundation that remains vulnerable.

Those crops, like the maize and wheat that feed the nation, require fertiliser.

And that fertiliser, for now, remains subject to the whims of global markets and the stability of distant shipping lanes.

What is required now is the focused implementation that transforms policy into production.

Reviving local fertiliser manufacturing is not a simple undertaking. It requires investment, technology, access to feedstock and the development of human capital.

But the alternative — continued dependence on imported fertiliser in a world where supply chains are increasingly weaponised and disrupted — carries risks that grow by the year.

By building domestic capacity, Zimbabwe could not only secure its own requirements but potentially emerge as a regional supplier, contributing to broader African food security while generating export earnings.

The timeline for action is constrained.

The time to build capacity is now, while global markets, though stressed, remain functional.

The National Development Strategy envisions an empowered, prosperous Zimbabwe.

That vision cannot be realised if the country’s agriculture sector remains perpetually vulnerable to external shocks.

The Russia-Ukraine war provided one wake-up call. The potential closure of the Strait of Hormuz provides another. It is, therefore, now time for local fertiliser manufacturing to move from policy document to concrete action.

The policy framework exists. The strategic imperative is clear. What remains is the will and investment discipline to transform aspiration into ammonia and strategy into substance.

The next planting season will come, and the one after that, and the one after that.

Each will arrive with the same question: Will Zimbabwe’s farmers have the fertiliser they need?

For too long, that answer has depended on factors beyond the country’s control.

However, the Local Content Policy offers a path to change that equation.

The time to walk that path is now.