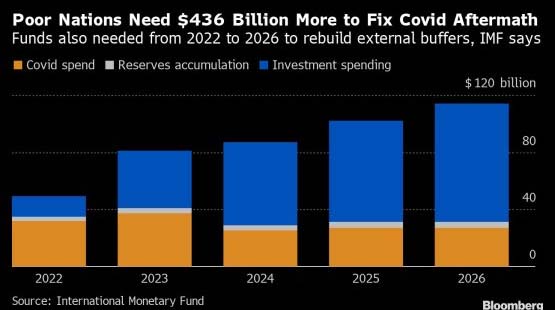

The world’s 69 poorest countries need an extra US$436 billion over five years to address the aftermath of Covid-19, rebuild external buffers and grow incomes, the International Monetary Fund (IMF) has said.

Of that amount, US$170 billion is to tackle the effects of the pandemic, such as loss of learning and worsening poverty, and bolster reserves.

The rest is required to help low-income nations catch up with emerging markets’ average ratio of spending relative to gross domestic product by 2026, the Washington-based lender said in a report released on Thursday.

“The compound shocks from the pandemic and Russia’s war in Ukraine have disproportionately affected low-income countries,” the fund said.

“They now face the challenge of resuming income convergence against

the backdrop of a weak and uncertain global economic environment.”

Poor nations are reeling from inflation, higher interest rates and elevated food and energy costs, while dealing with record debt levels, climate change and either slow growth or recession.

IMF calculations show that about one-third of the world economy will have at least two consecutive quarters of contraction this year and next, and that the lost output through 2026 will be US$4 trillion.

Surging prices have forced central banks worldwide to tighten monetary policy, and the Federal Reserve’s aggressive stance has supercharged the dollar.

Meanwhile, developing nations have amassed a quarter-trillion-dollar pile of distressed debt that threatens to create a historic cascade of defaults. The 69 countries — which the IMF defines as those that are eligible for funds in its Poverty Reduction and Growth Trust — have lost several years of progress towards achieving the United Nations’ sustainable development goals in areas such as poverty and education. Most of them are in Africa.

“With greater challenges under more constrained resource envelope, removing structural barriers to sustained and inclusive growth

has become ever more important,” the IMF said in a statement accompanying the report.

Policymakers “should wield all instruments available” to fight inflation, protect the vulnerable, preserve growth, contain debt vulnerabilities and manage financial-sector risks, the fund said.

It added that countries should be mindful of maintaining credible fiscal and monetary policy frameworks and not lose sight of longer-term issues, like poverty, inequality, climate change and digitalisation. — Bloomberg