Tawanda Musarurwa in BEIJING, CHINA

FROM Beijing, it is easy to think about the vendor back home who always had maybe 30 seconds.

She would bundle her tomatoes into a chitenge cloth and move fast west on Julius Nyerere, then into an alley off Inez Terrace before the municipal police truck turned the corner. The officers never bothered running. They had been there before. So had she.

“Vaenda neuko” — “They have gone that way” — would pass mouth to mouth along the stalls in seconds.

By the time the truck circled back, the pavement would be empty. The economy had made itself invisible again.

Zimbabwe has been having this argument with its informal sector for decades. The tools keep losing. You cannot collect tax from someone who takes cash, keeps no records and can easily vanish.

But, the phones in the pockets of those same vendors — running EcoCash, paying for airtime and ordering stock via WhatsApp — are generating data. And a modern tax administration runs on data.

The country now faces two distinct problems at once. Millions of citizens operate outside formal tax systems on the street.

And billions of dollars of new economic activity — online businesses, remote workers, e-commerce and digital services — move through channels that traditional tax law was never built to catch. The technology creating the second problem may be the only practical solution to the first.

The Zimbabwe Revenue Authority (ZIMRA) knows this. Its 2026–2030 strategic plan puts digital transformation at the centre of everything: less manual enforcement, more data and more intelligent systems.

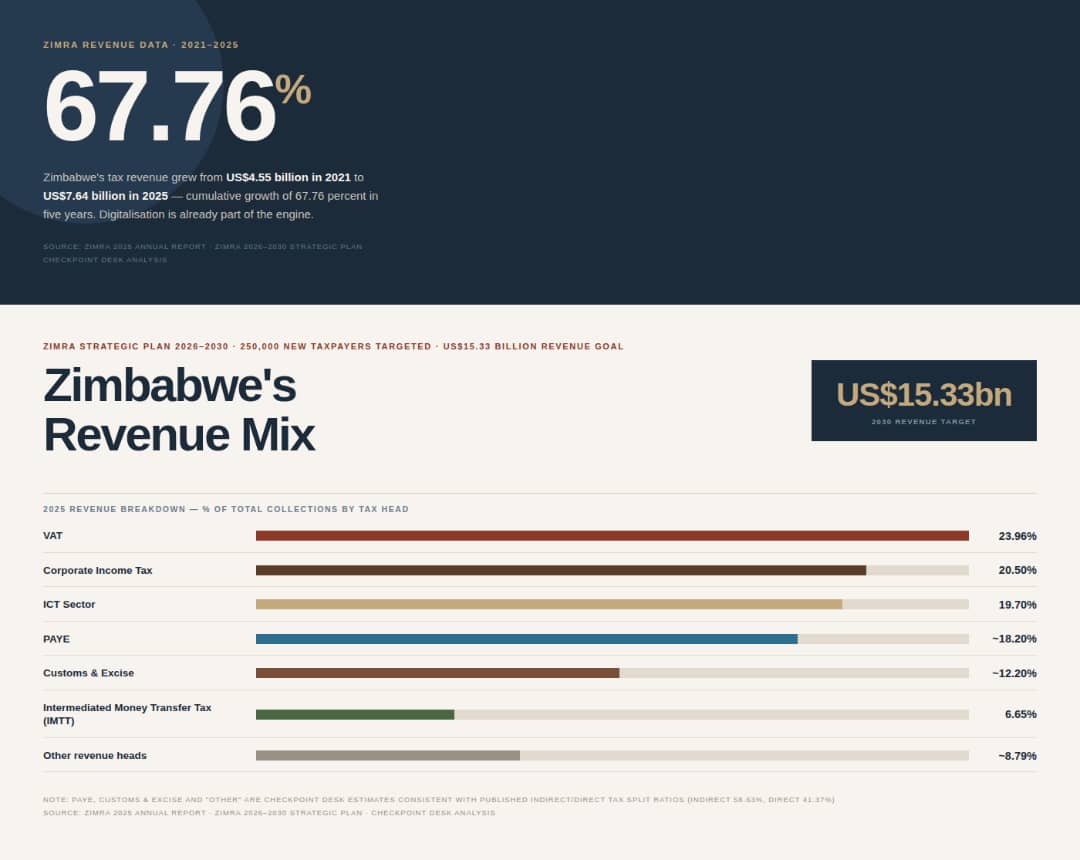

Official data from ZIMRA show that revenue collections rose from the equivalent of US$4,55 billion in 2021 to US$7,64 billion in 2025 — cumulative growth of 67,76 percent over five years. Digitalisation is already part of the engine.

A Beijing classroom, a Zimbabwean problem

On June 23, a delegation of Zimbabwean fiscal officials sat in the now familiar lecture hall at the Central University of Finance and Economics (CUFE) in Beijing. The subject was tax and the digital economy.

Professor He Yang of CUFE’s School of Taxation did not offer much comfort.

Two days earlier, Professor Qiang Ren, also of CUFE, had framed the broader stakes. China’s rise, he argued, was not built on factories and export industries alone — it required the simultaneous rebuilding of the fiscal architecture that funds development.

The lesson for Zimbabwe was not to replicate China’s tax system, but that successful economies build tax systems that grow alongside industrialisation, technology and business expansion. Delay that work, and the cost compounds.

Digital firms, she explained, can serve foreign markets without creating the traditional taxable presence — the “permanent establishment” — that triggers a tax liability.

A company renting webspace and a telephone number in another country has no taxable nexus there. It keeps every dollar.

She walked the delegation through a case study: a construction company building a factory abroad for 13 months creates a taxable presence because the treaty threshold is 12 months. A virtual office providing services remotely creates nothing. The same treaty, but different outcomes.

As businesses move online, more and more of them look like the second case.

The deeper problem is data. The professor quoted a line that has circulated widely in tax policy: “The world’s most valuable resource is no longer oil, but data.”

Digital companies extract enormous value from their users — who provide that data for free — then locate the resulting profits in low-tax jurisdictions.

While the customers in the market country generate the value, the tax goes elsewhere.

China has spent years trying to fix this domestically.

Under its new VAT law, taking effect in 2026, overseas businesses selling into China face withholding obligations regardless of physical presence.

Online platforms — retail, livestreaming, freight, education, AI-generated content — must now report not just their own revenues, but those of every third-party seller operating through them. Identity data, revenue data, transaction records. This is visibility, built by law, one platform at a time.

Professor He was careful not to hold China up as a template. The 1994 tax-sharing reforms that modernised China’s fiscal architecture took a generation to produce results. China’s tax-to-GDP ratio fell from 22,8 percent in 1985 to 12,29 percent by 1993 before the reforms stabilised it.

Her central warning was that countries that delay building proper fiscal infrastructure pay for it in lost revenue for decades.

For Zimbabwe, it landed with some weight. Official figures show that the country’s ICT sector was already the second-largest revenue contributor in 2025, accounting for 19,70 percent of total collections.

As that share grows, the question of which rules govern its taxation stops being theoretical.

The street trader and the digital platform

Back in Harare, the practical version is easier to see. Take a property owner who has converted an office block in the CBD into a mini-mall — dozens of small spaces rented to traders at US$300 a month, all cash.

The owner collects thousands of dollars monthly. The economic activity is real. The tax system cannot easily see it.

Digitising that rental payment — moving it to mobile money — creates a record. Not necessarily to tax every small trader immediately, but to understand the income flows and start the process of bringing significant earners into compliance. The first step is visibility.

ZIMRA’s 2025 Annual Report is direct about the scale of the problem: businesses operating outside formal frameworks, transactions in cash, limited records and no registration.

“This creates an uneven playing field between formal and informal sectors,” read part of the report. It is also a large hole in the revenue base.

The country’s own VAT data shows what happens when digital administration reaches activity that was previously opaque.

The figures show that VAT was the largest single revenue source last year, contributing 23,96 percent of total collections.

ZIMRA attributes part of the improvement to the Fiscalisation Data Management System and increased use of electronic payments. When transactions become traceable, compliance improves because the system can see them.

Mobile money tells the same story. Intermediated Money Transfer Tax contributed 6,65 percent of total revenue in 2025, exceeding its target by 62,06 percent.

ZIMRA links that directly to growth in electronic payments. Digital activity created digital taxability.

Doubling revenue without squeezing the same people

ZIMRA’s plan targets US$15,33 billion in revenue by 2030 — nearly double the 2025 figure. That can be achieved by enlarging the tax base.

The plan sets a goal of 250 000 new taxpayers registered between 2026 and 2030.

Whether that is achievable depends on whether the digital infrastructure exists to identify people and businesses currently outside the system — and to make formal participation easier than avoidance.

There is also a structural argument in the numbers. In 2025, indirect taxes — VAT, excise, customs, IMTT — contributed 58,63 percent of total revenue; direct taxes 41,37 percent. That balance reflects a large informal sector as indirect taxes are easier to collect where income records are thin.

Advanced economies tend to lean more on direct taxation because they have deeper formal bases. The direction of Zimbabwe’s tax mix is inseparable from the direction of formalisation.

Experts say a growing economy should expand the tax base, not increase pressure on the people already inside it.

In July 2025, Zimbabwe signed the Multilateral Convention on Mutual Administrative Assistance in Tax Matters, becoming the 151st jurisdiction to join the framework. That matters because cross-border digital commerce — and the profit-shifting Professor He described in Beijing — requires information exchange between tax authorities to counter. Without visibility across borders, national tax agencies fight blind.

The last piece

Professor He’s lecture touched on something that does not appear in any revenue table. Automatic compliance, AI-powered administration and platform reporting requirements are instruments. What they amplify depends on what already exists between taxpayers and the institutions collecting from them.

In Zimbabwe, that relationship carries real damage — from years of currency instability and uneven service delivery.

As it stands, every enforcement mechanism hits more friction than it should.

ZIMRA Commissioner General Ms Regina Chinamasa described the past five years in the 2025 Annual Report as demonstrating “institutional resilience, strategic focus and the Authority’s expanding capacity to support national fiscal stability.”

The numbers support that, but citizens need to feel it.

Rebuilding the relationship between citizens and the tax system — making visible not just who pays but how the money is used — is as important as any platform reporting law or digital PE reform.

The vendor along Julius Nyerere is not just a compliance problem. She is a signal about the distance between the formal economy and the people who live outside it.