Tawanda Musarurwa

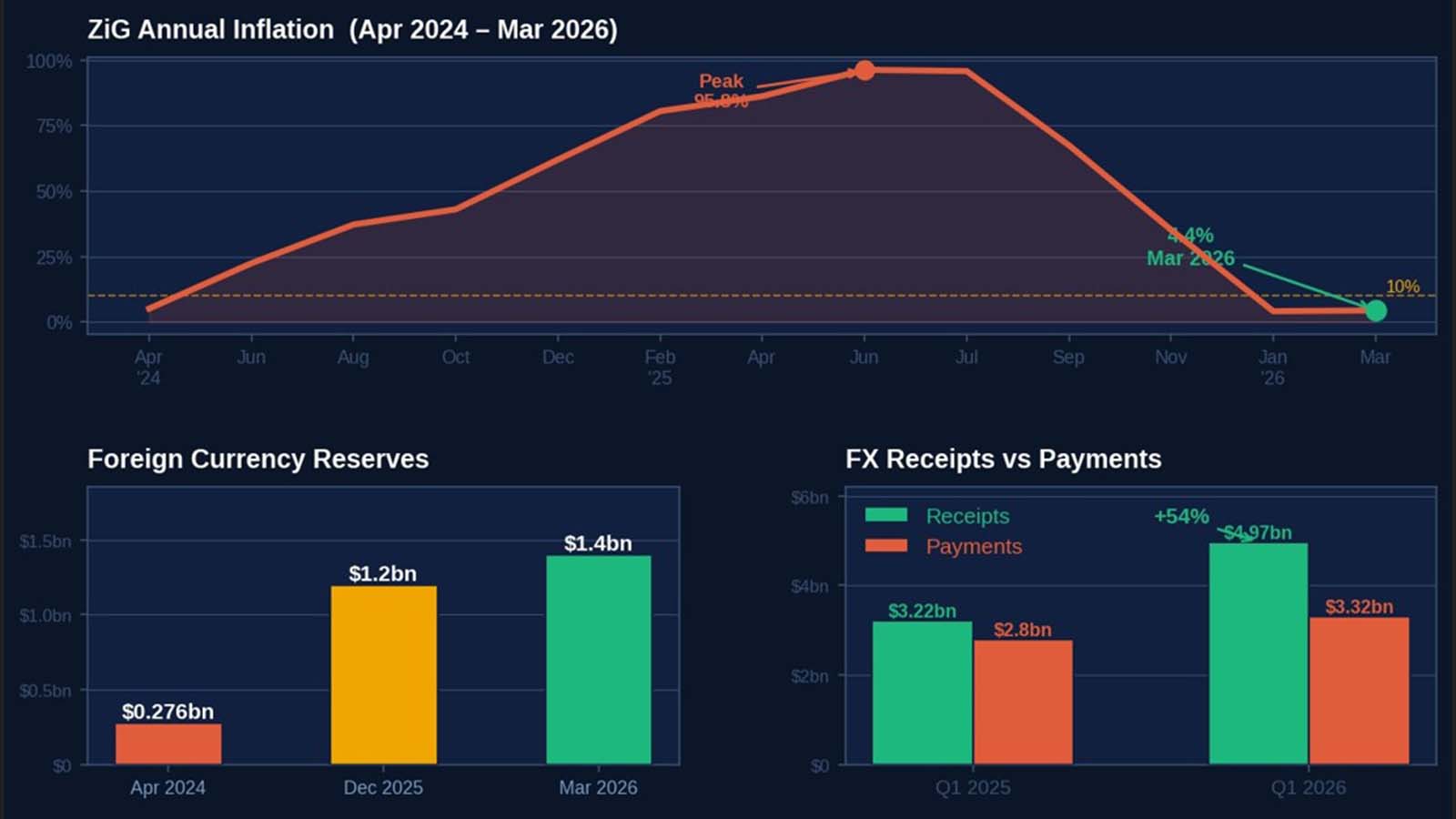

FROM 95,8 percent in July 2025 to just 4,1 percent six months later, Zimbabwe’s inflation story has taken a dramatic turn.

This sustained, verified disinflation that the Reserve Bank of Zimbabwe (RBZ) acknowledges – in its recent Q1 2026 Snapshot – has not been achieved in over three decades.

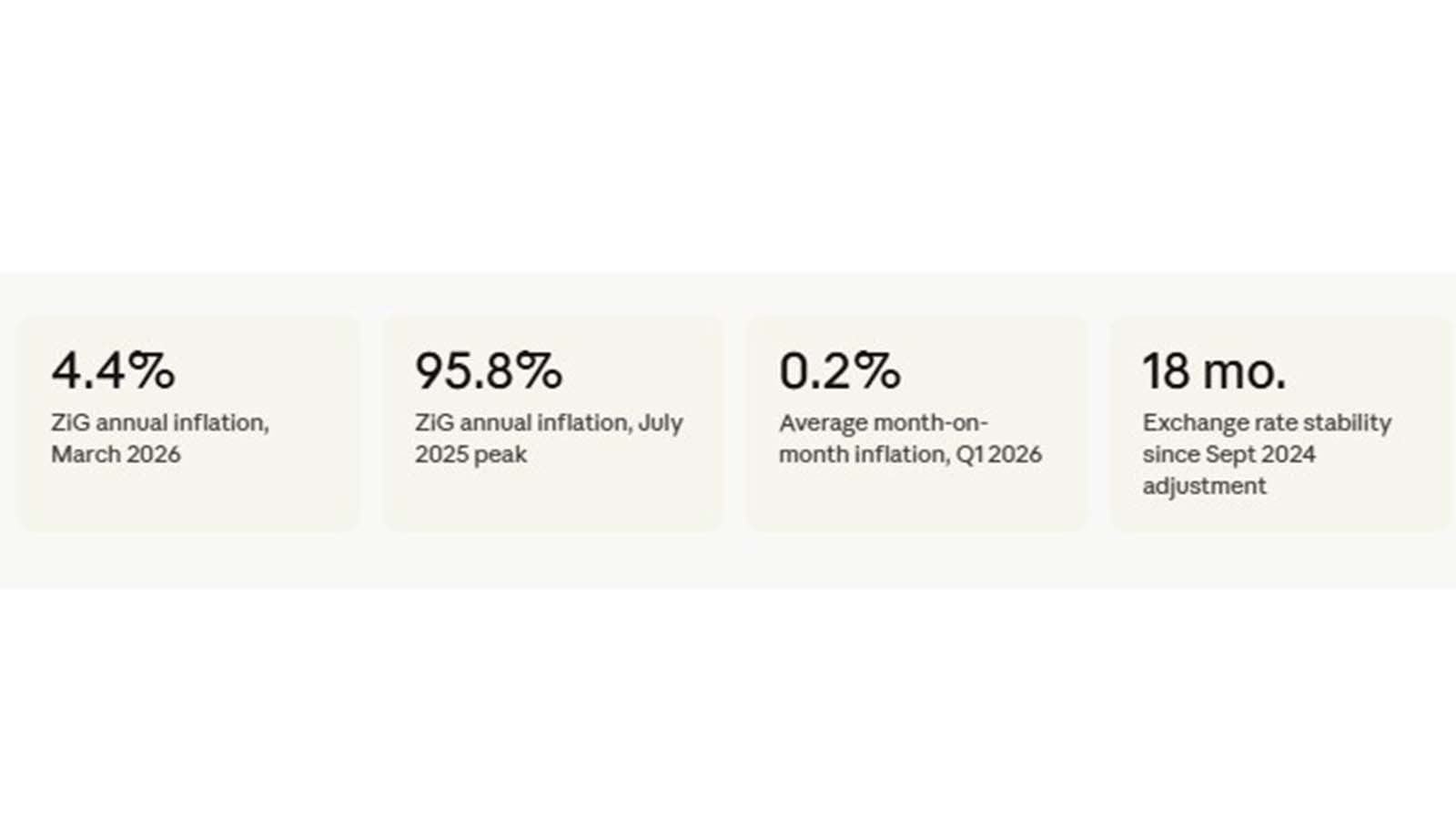

As at the end of last month, annual inflation stood at 4,4 percent. Month-on-month inflation across the first quarter averaged just 0,2 percent.

To understand why these are extraordinary figures, consider where the journey began: annual ZiG inflation peaked at 95,8 percent in July 2025.

In less than seven months, the central bank compressed that to single digits. The speed of that disinflation is, by any global comparison, remarkable.

The story behind those numbers begins not in 2026 but in April 2024, when the ZiG was introduced and foreign currency reserves stood at just US$276 million – barely enough to breathe.

The RBZ made one clear bet: that an aggressive, transparent and sustained build-up of hard currency backing could, over time, convert scepticism about a new local currency into something resembling institutional trust.

The data suggests that the bet is paying off. By March 31, 2026, foreign currency reserves had grown to US$1,4 billion – a more than fivefold increase in under two years.

Those reserves now cover approximately 1,5 months of imports, provide around six times coverage of ZiG reserve money, and back nearly double the entire stock of ZiG deposits in the banking system.

The 2026 Monetary Policy Statement is unambiguous about what this means: the reserves are not a precautionary buffer. They are the architecture of exchange rate credibility.

The interbank exchange rate has oscillated between ZiG25 and ZiG27 per US dollar since that once-off market-driven adjustment in September 2024.

The parallel market premium – historically a reliable barometer of how little Zimbabweans trusted their currency – has been held below 20 percent for most of Q1 2026, down from spreads that historically reached triple digits during previous currency crises.

The real effective exchange rate, a more sophisticated gauge of whether the currency is fairly priced relative to trading partners, has remained stable around its benchmark level.

Foreign currency receipts tell a complementary story.

Total inflows for the first quarter of 2026 reached US$4,97 billion – a 54,1 percent increase on the US$3,22 billion recorded in the same period last year.

Export earnings dominated, contributing 71 percent of the total, driven by gold, tobacco, platinum group metals and lithium.

Diaspora remittances added 14,8 percent. The surpluses these inflows generated – US$109,9 million in January, US$46,4 million in February – shifted Zimbabwe’s current account from a US$19,7 million deficit in Q1 2025 to a projected surplus of over US$590 million in Q1 2026.

That is a structural shift.

The cumulative picture since April 2024 is even starker. Total foreign currency receipts over that period: US$32,7 billion.

Total payments: US$19,67 billion. The difference – US$13 billion – represents the foreign exchange surplus that has funded both reserve accumulation and the smoothly functioning domestic foreign currency market. The arithmetic of stability, laid bare.

How has the RBZ managed inflation itself?

The policy toolkit is more sophisticated than it might appear. The bank policy rate has been held at 35 percent – a deliberate choice, not a default.

The 2026 MPS is explicit: achieving single-digit inflation creates the conditions for eventual rate cuts, but premature easing risks reversing gains accumulated over three hard years.

“Any renewed inflation pressures,” the MPS warns, “have the potential to induce policy reversals, including necessitating an even more aggressive tightening, with higher economic and social costs.”

The rate stays where it is until the data says otherwise.

There are headwinds. The RBZ acknowledges that oil price shocks – tied to geopolitical tensions – will likely push annual inflation temporarily higher through to June 2026 before it returns to steady state.

The bank policy rate was held at 35 percent at the March MPC meeting specifically to contain these second-round effects.

The economy grew, despite a mid-season agricultural dry spell, and is projected at 5 percent growth for 2026 – suggesting the tight monetary stance has not choked the real economy, at least not yet.

The deeper context matters too. Zimbabwe and the IMF reached a Staff-Level Agreement under a 10-month Staff-Monitored Programme.

The current monetary framework directly informed the SMP’s parameters. External accountability of this kind is new for Zimbabwe; it adds a layer of credibility that domestic policy commitment alone cannot fully provide.

Local currency constituted just 18 percent of total money supply at end-2025. The road to Zimbabwe’s stated 2030 mono-currency goal is long, and the data shows it plainly: US dollars still dominate.

But, the direction of travel – confirmed by the ZiG’s usage in the National Payments System rising to a peak of 43 percent in May 2025 and averaging 35 percent to 40 percent for most of the year – is one the numbers have not previously supported.

For the first time in a generation, they do.

4,1 percent in January. 3,8 percent in February. 4,4 percent in March. Three data points, 30 years in the making.