Golden Sibanda

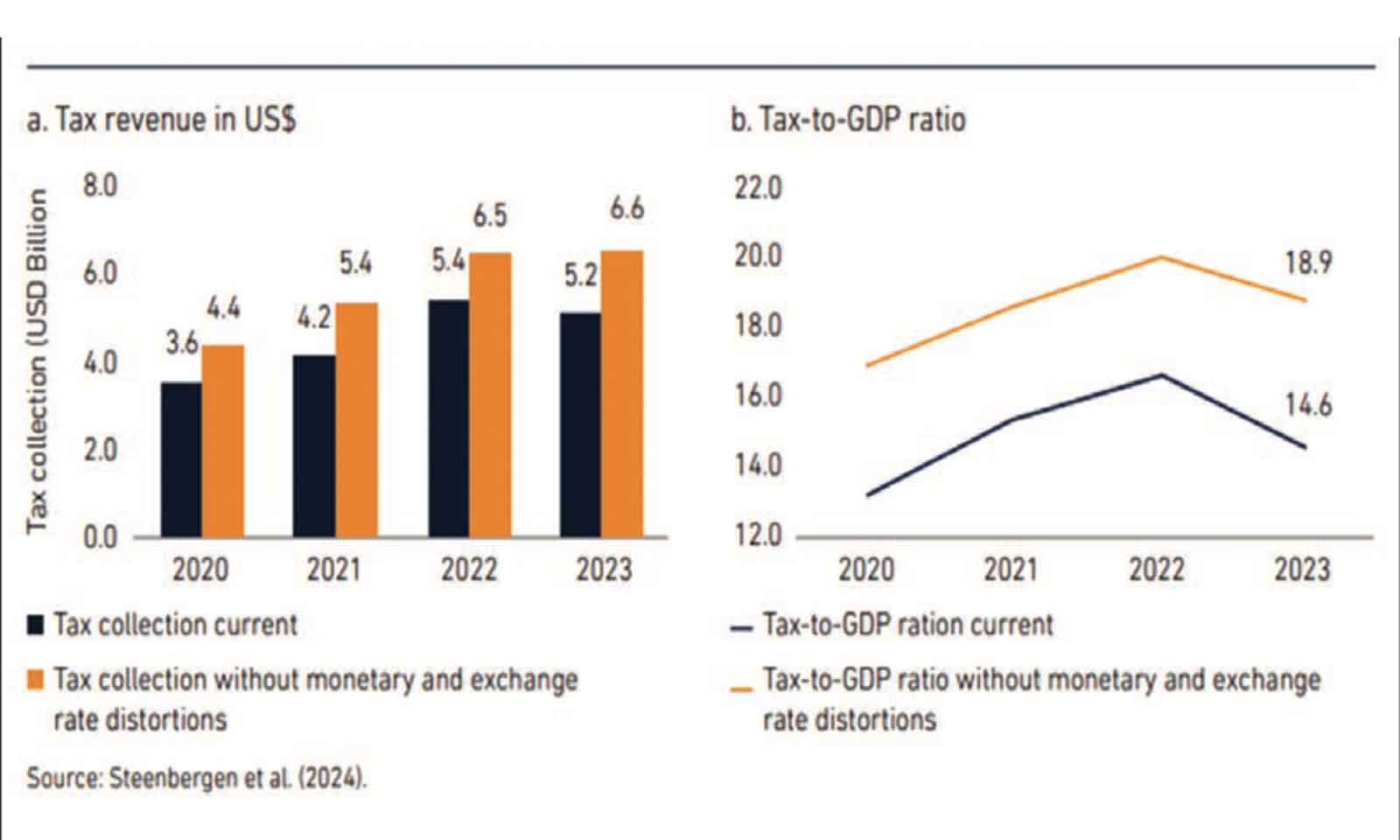

Zimbabwe’s Treasury may have lost a cumulative US$4,5 billion due to monetary and exchange

rate distortions between 2020 and 2023, the World Bank said in a report released this week.

The global lender also suggested that without the distortions, Zimbabwe’s tax revenue could have been as high as US$6,5 billion in 2023.

in a Public Finance Review (PFR) report of Zimbabwe’s fiscal operations, the multilateral lender said Zimbabwe’s monetary and exchange policies thus resulted in a major re-distribution from the Treasury toward the RBZ.

Zimbabwe has had to rely on innovative domestic sources of financing since the turn of the millennium, when multi- lateral lenders cut concessionary funding over arrears while Harare’s fallout with Britain, closed many avenues to bilateral and foreign financing.

The fallout, after Zimbabwe repossessed land occupied by white former commercial farmers, to resettle the land- less majority, western nations led by Britain and America, imposed a coterie of economic and travel embargoes on the country’s key state actors and institutions.

The southern African nation has not been able to access concessional loan funding from multilateral lenders while the sanctions also collapse virtually all correspondent banking relationships, making access to foreign funding difficult, if not impossible.

But the domestic financing strategies inadvertently had their fair share of undesired consequences, including increasing money supply, exchange rate volatility and inflation rampage.

The World Bank said as the central bank reportedly printed money to finance Quasi-Fiscal Operation (QFOs), gains from the RBZ through seignior- age and international loans, came at the expense of the Treasury, through the loss of tax revenue and increased indebted- ness.

The QFOs occurred in two distinct ways based on the currency and financing method, including Zimbabwe dollar-denominated QFOs driven by the RBZ directly printing money to lend to the Government.

“This was notably done from 2004 to 2007, resulting in hyperinflation in 2008 (munoz, 2007).

“US dollar-denominated QFOs are con- ducted in two separate ways: (a) servicing US dollar-denominated expenditures with Zimbabwe dollar.

“To provide US dollar-denominated expenditures, the RBZ borrowed US dollars from offshore commercial lenders, who were repaid through Zimbabwe money creation.

“(b) Repaying US dollar export surrenders in Zimbabwe. The RBZ also maintains a surrender requirement that obliges exporters to exchange a share of their US-dollar receipts to the RBZ in exchange for local currency.

“Rather than reselling this forex in full via a domestic foreign currency auction, it utilised a part to service its own US dollar-denominated debt and paid for such US dollar export surrenders through Zimbabwe money creation.

US dollar-denominated QFOs reportedly resulted in exchange rate depreciation, leading to a vicious cycle where increasing amounts of Zimbabwe dollars needed to be printed to service US dollar-denominated loans or US dollar-ex- port surrenders.

“This also ultimately undermined the GoZ’s (Government of Zimbabwe) ability to finance its development objectives, as the RBZ’s gains (+3,1 percent of GDP) were lower than the losses to the Treasury (-5,5 percent of GDP).

“This again confirms findings from Cagan (1956) and Tanzi (1978) that, while policymakers may consider monetary and exchange rate distortions beneficial in the short run, they ultimately cause significant revenue losses in the medium

term that are often less visible,” the bank said.

The global lender said Zimbabwe’s monetary policy has been defined, in large part, by quasi-fiscal operations (QFOs). QFOs are the financing of the Government, state-owned enterprises (SOEs), and private sector companies by the central bank, often through money printing.

“The RBZ has historically been deeply involved in QFOs through printing money

and using this to finance external debt servicing payments, supporting SOEs, and making transfers to the real sec- tor through agricultural subsidies and incentives for gold production (World Bank, 2023).

“The RBZ has engaged in QFOs to make payments in both (Zimbabwe dollars) (through direct Zimbabwe dollar loans) and in US dollars (by borrowing from international commercial lenders, and by exploiting export surrender requirements),” the world bank said.

The RBZ’s QFOs, the world bank said, led to a big increase in the Zimbabwe dollar money supply, which resulted in high inflation and rapid deprecation of the exchange rate.

Growth in reserve money is closely cor- related with Zimbabwe’s inflation, and big spikes in reserve money resulted in periods of high inflation in the summer of 2020 and 2023.

According to the multilateral lender, a close-to-perfect linear relationship exists between the money supply and the Consumer Price index (CPI). excess money sup- ply also undermines the value of the local currency, leading to rapid depreciation.

This, in turn, also harms local prices as traders price-adjust to the new, lower exchange rate, thus importing inflation. as such, there is also a strong correlation between the CPI and the exchange rate.

In his 2025 monetary Policy Statement, RBZ Governor Dr John Mushayavanhu said the central bank would continue with the tight monetary policy stance, whose over-arching objective was to foster Central bank policy credibility and trust under the back- to-basics strategy.

In that regard, he said the monetary pol- icy framework would be anchored on three interwoven strategic pillars articulated in the 2025-2029 Reserve bank Strategy Plan, which are consolidating price, currency and exchange rate stability, enhancing monetary stability, research, policy and data integrity and maintaining the safety, soundness and integrity of the financial sector.

Dr Mushayavanhu has since vowed that quantitative easing or money printing would not be permitted while he was in charge of the central bank.

“I don’t believe in quasi fiscal activities. it’s not going to happen under my watch. my mandate as spelt out in the Reserve bank act is very clear and i’ve no intention whatsoever to do other people’s jobs.

“I’ll do my job as the central bank Governor as defined in the act. in that respect, we’ve moved all quasi-fiscal obligations to Treasury in an effort to clean the balance sheet of the central bank,” Dr Mushayavanhu said in his maiden monetary Policy Statement in 2024.