Tawanda Musarurwa-Checkpoint Desk

FOR decades, technology promised to make users’ work simpler; faster claims, quicker service and fewer mistakes.

But, with the rise of artificial intelligence, the promise is not so simple.

The race is no longer just for smarter systems, but for bigger ones — data-hungry, power-thirsty and costly to the planet.

The United Nations Environment Programme (UNEP) warns that the global AI boom carries hidden environmental costs.

“The proliferating data centres that house AI servers produce electronic waste. They are large consumers of water, which is becoming scarce in many places,” UNEP noted in its 2024 report.

“They rely on critical minerals and rare elements, which are often mined unsustainably. And they use massive amounts of electricity, spurring the emission of planet-warming greenhouse gases.”

In parts of Asia and North America, sprawling data centres have strained local grids and drained water resources, forcing nearby communities into rationing.

Against this backdrop, as global players race to scale up, can Zimbabwe’s AI adoption be smaller, local and sustainable?

This question is particularly pressing in the insurance sector, where enthusiasm and need for AI is rising, even as the foundations to support it remain fragile.

An interesting fix

Faced with limited data and unreliable infrastructure, the local insurance sector is seeking smaller, smarter fixes.

In 2024, the Insurance Council of Zimbabwe (ICZ) took a step toward addressing this problem through its annual research competition.

The winning entry announced earlier this year, developed by University of Zimbabwe student Augustine Mupeti, was a prototype he called the “Bexman clustering algorithm.”

Instead of relying on vast datasets like those used in global insurance firms, Mupeti’s model applies “churn clustering” — grouping customers by behavioural similarity — to work effectively with limited data.

“While some data is being generated, the total amount is often not enough for sophisticated AI models,” he said.

“A bank might have transaction histories, but no data on online behaviour or phone usage. This incomplete data prevents the AI from finding hidden clues.”

The unique algorithm, which Mupeti practically demonstrated during the competition, can be used for various applications such as customer segmentation, churn clustering, fraud detection and community detection, which make it ideal for the insurance sector, but also for other industries.

Mupeti’s innovation exists within a wider national context; one where data appears scarce.

The local insurance sector’s dependence on motor insurance — which accounted for 88 percent of all active policies and roughly 66 percent of total insurance revenue in the second quarter of this year, according to the Insurance and Pensions Commission’s (IPEC) 2025 Q2 report — illustrates both its stability and its fragility.

AI models trained only on such skewed datasets risk overlooking entire customer groups, especially low-income or rural clients with different risk patterns.

“Limited historical data makes actuarial product design complicated,” said AFC Insurance CEO Mr Cuthbert Masukume, while discussing innovating around agricultural index-based insurance.

Localised algorithms like Mupeti’s, designed to work with smaller, incomplete datasets, could therefore help bridge this digital asymmetry.

Digital blind spots

According to Postal and Telecommunications Regulatory Authority of Zimbabwe (Potraz) data, the country’s penetration rate stood at 81,49 percent — around 12 million Zimbabweans — as at the end of last year.

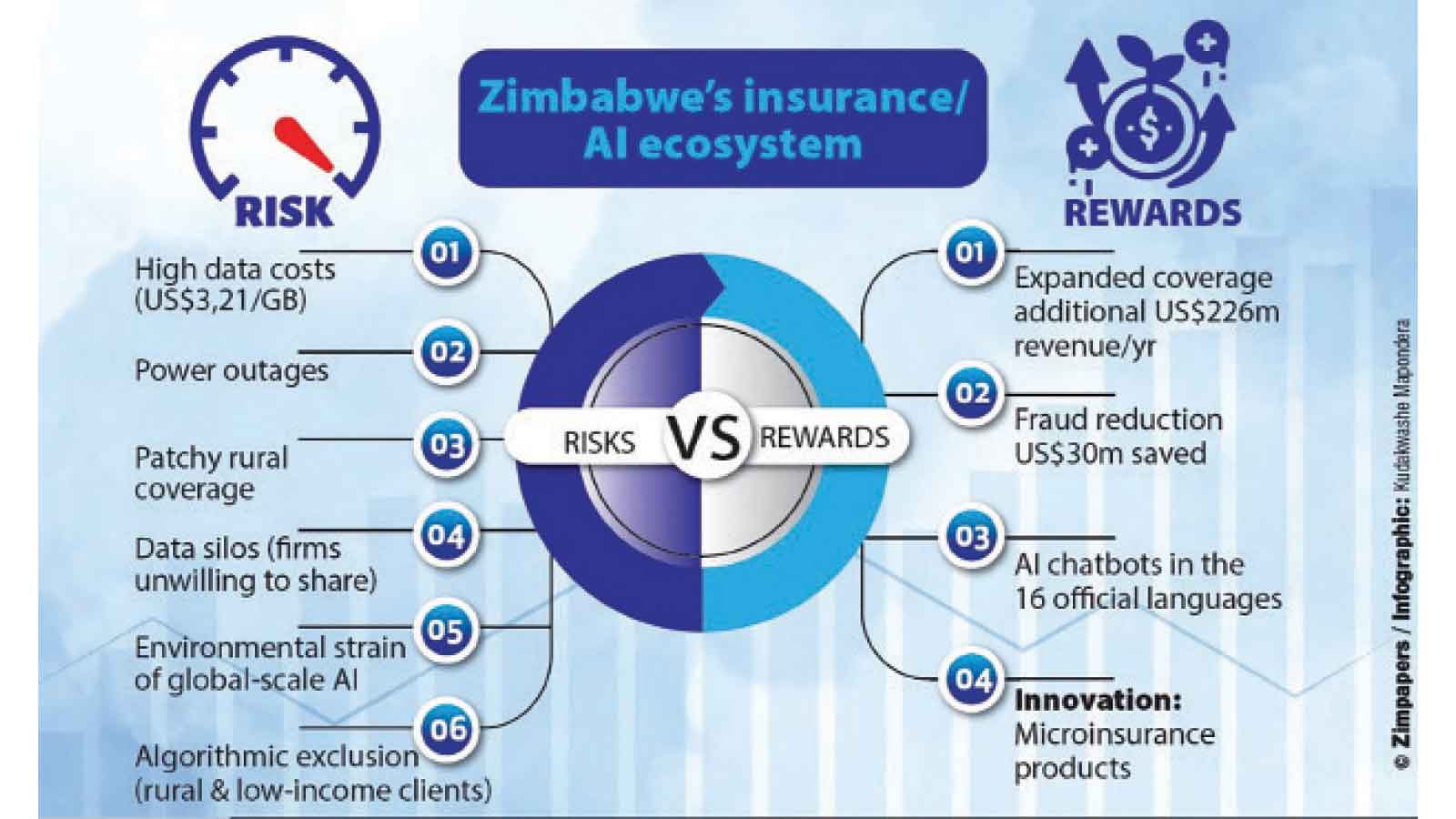

Mobile internet dominates, but at US$3,21 per gigabyte (according to Potraz), data in the country is expensive relative to income.

Power outages and patchy network coverage, especially in outlying areas only deepen the divide.

For insurers, this means fewer digital trails to analyse and when the data is not there, AI has little to work with.

Imagine a 47-year-old farmer who buys a weather-indexed crop insurance policy. When drought hits, the AI system meant to verify her losses fails to register the damage, simply because she rarely uses a smartphone.

In this scenario, she is told the data does not match, even though her crop is affected, leaving her unaccounted for.

These gaps are not just technological; they are structural and they complicate both innovation and regulation.

Regulations are coming, slowly

Government is beginning to respond to these emerging challenges.

Earlier in October, Cabinet approved the National Artificial Intelligence Strategy aimed at harness the economic potential of artificial intelligence, which is aligned with the broader Smart Zimbabwe 2030 Master Plan.

The regulator, too, is pushing for innovations.

IPEC has introduced “regulatory sandboxes” — controlled environments for testing AI-driven products without exposing consumers to undue risk.

“The successful implementation of this regulatory sandbox framework will position Zimbabwe as a progressive market for insurtech, attracting investment and expertise, ultimately benefitting consumers through tailored and accessible insurance solutions for the Zimbabwean populace,” said IPEC in its 2024 annual report.

However, policy, as it always does, is playing catch-up. There is no insurance-specific AI rulebook and deeper issues remain unsaid. For instance, who owns customer data — the insurer, the client or the state?

Such uncertainties add pressure to an already shallow market.

A market too small to ignore

According to IPEC, Zimbabwe’s insurance penetration rate — premiums as a share of gross domestic product (GDP) — stood at around 2 percent in 2024, broadly unchanged from recent years but still well below levels seen a decade ago.

By comparison, Kenya stands around 2,3 percent, Nigeria 0,45 percent and South Africa around 12 percent.

The global average is roughly 7 percent.

The country’s thin market reflects underlying fragilities, but it also marks out one of the economy’s clearest avenues for future growth.

With the right tools, insurers could reach untapped segments. AI can help lower costs, personalise products and deliver services through mobile applications or chatbots in local languages.

Fraud, however, remains a major drain. Industry estimates suggest that 25 percent to 30 percent of total payouts are fraudulent, costing insurers roughly US$80 million to US$100 million annually in a market where total insurance revenue reached US$452 million last year.

Local technology firm Mugonat Systems has begun integrating AI-based anomaly detection into insurer workflows.

“We are pioneering the adoption of AI in the local insurance industry, incorporating advanced technologies into their existing solutions for medical aid and short-term insurance,” said Mugonat Systems CEO Mr Tendai Mugovi.

A single percentage-point drop in fraud losses could save companies millions.

Sparks of progress

There are glimmers of momentum.

The ICZ Research Competition, offering awards of up to US$4 000, has spurred practical innovation.

Second, a farmers’ insurance pilot launched in Goromonzi last October and later expanded nationwide, showing how targeted products can reach rural clients; it is a model that AI could refine further.

And at the broader level, microinsurers — often seen as the industry’s experimental frontier — are quietly expanding access. Their policy base grew to 124 000 active policies in Q2, 2025, with 67 percent of their business written in US dollars. Legal aid and funeral cover dominate, but new products like credit and farming insurance surged 187 percent and 148 percent, respectively.

With appropriate AI tools for segmentation and pricing, these high-growth microsegments could become the foundation of a more inclusive insurance system. But, for AI to scale responsibly, it needs more than just good ideas, but also good data.

What “good data” looks like

To make AI work, insurers need both data volume and quality, such as reliable records on transactions, online behaviour and phone use. Accuracy is crucial.

An algorithm trained on patchy information will misprice risk and miss fraud.

Digital transformation strategist Dr Dennis Magaya, however, argues that many local firms are just reluctant to open up their data, a hesitation that could hinder meaningful AI adoption.

“Licensed entities like insurance, banking and telecoms have lots of data which can help in AI deployment,” he said.

“They have data, but perhaps not willing to share it.”

Inclusivity matters too, because if chatbots fail to grasp local languages (Zimbabwe has 16 official languages, including English) they risk serving urban elites, while leaving minority communities behind.

Observers say for artificial intelligence to move from promise to practice, four key pillars must align.

First, ethical regulation must extend beyond experimental sandboxes to encompass fairness, accountability and should be easy to understand.

Second, robust infrastructure – including reliable power and broadband – is essential to sustain the data operations that underpin AI systems.

Third, skills retention is critical; Zimbabwe must not only train but also retain its scarce pool of machine-learning talent.

Finally, public trust must be cultivated, with insurers ensuring transparency so that customers clearly understand how algorithmic decisions are made.

The payoff could be huge. An increase from 2 percent to 3 percent in the country’s insurance penetration rate would imply insurers’ annual total revenue of about US$678 million, an increase of roughly US$226 million.

A 10 percent reduction in fraud losses could free around US$30 million, enough to expand rural microinsurance by several million policies.

But, as with any powerful tool, AI carries risks, particularly for those least able to absorb them.

When algorithms hurt the vulnerable

But, the dangers are real.

A poorly-tuned or misfiring model could reject a widow’s claim without explanation.

“The danger is that AI becomes just another elite toy,” warns Mr Nhamo Mudzonga, a policy analyst. “If rural people are excluded again, then what’s the point?”

Opaque systems could deepen mistrust toward insurers. And with weak data protection, privacy breaches could surge.

For regulators still catching up with paper-based fraud, policing algorithmic decision-making will not be easy. The country’s insurers now stand at a fork in the road.

With innovations like Mupeti’s algorithm and a new national AI strategy, insurers could leapfrog into a smarter, more inclusive future.

But, without stronger data, steadier power and deeper trust, their algorithms risk becoming what one claims officer called “sleek laptops in a blackout; impressive, but useless.”