Business Reporter

ZIMBABWE’S pension funds are increasingly favouring investing in property over stocks, marking a notable shift from traditional asset allocation, where equities typically held the largest share.

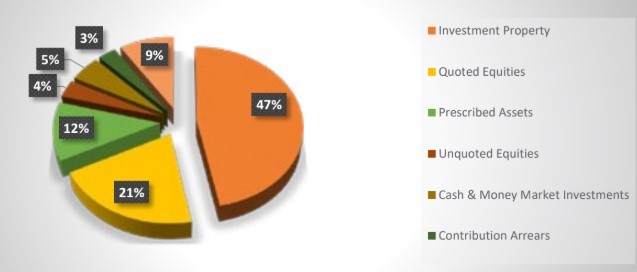

According to the Insurance and Pensions Commission (Ipec) fourth-quarter 2024 report, the pension industry’s assets were predominantly concentrated in investment properties at 47 percent and quoted equities at 21 percent of the total asset portfolio.

Conversely, as at December 31, 2018, quoted equities contributed 47,1 percent, while investment property was 21 percent of total assets.

The latest report indicates that as at December 31, 2024, the value of investment properties rose by 6,9 percent to US$1,06 billion (ZiG 27,4 billion), up from US$990 million.

At the same time, the value of quoted equities marginally declined by 0,5 percent in US dollar terms, from US$466,1 million on December 31, 2023 to US$463,7 million (ZiG11,96 billion) on December 31, 2024.

However, while the value of investment properties increased, the proportion of this asset class relative to total assets declined to 47 percent from the 50 percent reported in the corresponding period a year earlier.

The share of quoted equities to total assets also suffered a decline, with the proportion of total assets falling to 21 percent from 23 percent in the prior year.

The decline was because of the All-Share Index slowing down towards the end of the year, according to Ipec.

Unquoted equity investments saw a significant increase of 19,6 percent, rising from US$66,2 million to US$79,2 million.

The industry’s prescribed asset investments also saw substantial growth, increasing by 47 percent from US$180,2 million on December 31, 2023 to US$264,4 million (ZiG6,8 billion), driven by revaluation gains and new acquisitions.

Safe haven and hedge

Zimbabwe’s property market is perceived as a safe haven for investors seeking long-term value and a means to hedge against inflation and preserve wealth within a dynamic economic environment.

Analysts suggest that the increased allocation to property by pension funds is driven by attractive returns, although they acknowledge that equities will always remain a crucial asset class.

IH Securities head of research Mr Lloyd Mlotshwa said the global portfolio allocation to property typically averages around 10 percent, with an aggressive weighting potentially reaching 20 percent.

“That clearly suggests an above-normal inclination towards property in our market. This is explained by our history of adverse monetary events linked to currency volatility and hyperinflation, which have decimated portfolios in the past,” he said.

“Bricks and mortar are favoured as a long-term currency hedge, and this will likely become more pronounced as we approach 2030 if concerns surrounding currency are not alleviated.”

Property, he also said, does present its own complexities.

An overallocation to property may negatively impact an investor’s liquid requirements.

“Sub-economic rental yields can also negatively impact valuations and cash flow. Rising vacancies and voids if location dynamics shift, similar to what has occurred in the central business district (CBD), also remain another significant risk,” he added.

The emergence of real estate investment trusts (REITs), Mr Mlotshwa added, was a positive development.

“This allows pension funds to blend the desire for capital preservation through real estate with the liquidity profile of equities, whilst receiving an assured dividend yield, which is effectively a disbursement of the rental income back to the investor,” he said.

According to the pensions report, pension funds’ investments in unquoted equities increased by 19,6 percent to US$79,2 million (ZiG2,04 billion) from US$66,2 million during the same period last year.

This resulted in an increase in the proportion of unquoted equities to total assets from 3,3 percent to 3,5 percent.

Economist Mr Malone Gwadu attributed the increase in property investment by pension funds to attractive returns from rental income and continuous revaluation gains.

“Therefore, the nature of this return aligns well with the investment objective of pensions, which is long-term investment returns that will then be able to cater for contributions when they mature,” he said.

“Furthermore, properties have demonstrated some resilience to market volatility, such as inflation and exchange rate movements, and this resilience has acted as a hedging instrument for pension funds for value preservation.”

Mr Gwadu, however, cautioned that concentration risk becomes a significant concern if pensions continue to heavily invest in properties, as they may become overexposed to the property sector and lack sufficient diversification in other sectors offering good

returns.

“There are high-return sectors such as stock markets, the mining sector and the banking sector . . . Whilst relatively riskier, they offer high returns, and the Public Investment Corporation in South Africa serves as an example of a pension fund-backed investment vehicle with assets beyond property, such as banks like Nedbank and Ecobank,” Mr Gwadu added.

“Pension funds possess the necessary financial strength, individually or through syndication, to capitalise on almost every sector due to their substantial capital base and the patient nature of their funding positions.”

Offshore investments

Pensions were also granted permission to invest offshore last year to safeguard some of the value held on behalf of members.

However, the uptake of this investment class has been low due to the complex procedures involved in investing offshore.

According to Imara Capital’s second-quarter 2025 strategy research note, following the approval by Ipec of offshore-designated instruments with an upper limit of 15 percent of fund values, they have been actively seeking suitable foreign assets for their clients.

Imara reported that in 2023, their fund managers identified an offshore-administered USD-denominated trade financing instrument managed by a multilateral institution.

“We applied for and received all the various applicable regulatory approval processes to place some of our clients’ funds in the paper. The asset has performed extremely well for our clients to date — earning above-inflation returns,” Imara said.

“For the 12 months up to the end of March 2025, the asset posted a competitive 9,8 percent real return.”

Following its initial offshore investment in the TDB ESATAF fund and as part of its ongoing efforts to preserve value and diversify portfolios, Imara added, it had identified an additional long-term offshore investment deemed ideal for some of its clients.

“While Ipec should be commended for approving this asset class, the modalities still require some adaptation, with the current setup still somewhat cumbersome and not appropriate for investments in certain asset classes.”

Investment analyst Mr Enock Rukarwa suggested that in situations where investment classes offering value preservation are limited, pension funds are inclined towards property investments.

“Offshore investments have presented higher yields, stability and limited market risks compared to local investments,” he said.

He said quoted equities remain strategic for diversification, value preservation and liquidity purposes.

However, since the introduction of ZiG, the stock market has generally been bearish.