Rumbidzayi Zinyuke Post Correspondent

THE Zimbabwean Government has for years been trying to come up with ways to improve the country’s competitiveness on the global market.While progress has been made, analysts say the country still has a long way to go before it can begin to trade competitively with regional partners.

The country has been persistently ranked poorly on the Global Competitiveness Report, the World Bank’s Ease of Doing Business Report and the Global Corruption Index, just to mention a few.

The Office of President and Cabinet has been in charge of implementing reforms with a view to attaining a ranking of below 100.

Government has also established a taskforce to spearhead the enactment into law of a number of Bills, as it seeks to accelerate the ease of doing business reforms.

However, the 2017 Competitiveness Report shows that Zimbabwe slipped one place to number 126 out of 138 while the country is now ranked 161 out of 190 countries on the Ease of Doing Business report. Zimbabwe was ranked 155 out of 189 countries last year.

This is an indication that although the reforms implemented have helped, there is still more that needs to be done to ease the environment of doing business.

Analysts say this can come about once the country addresses the many barriers that exist in the economy.

Access to finance remains the most serious barrier to doing business in Zimbabwe followed by restrictive labour regulations and expensive operating environment.

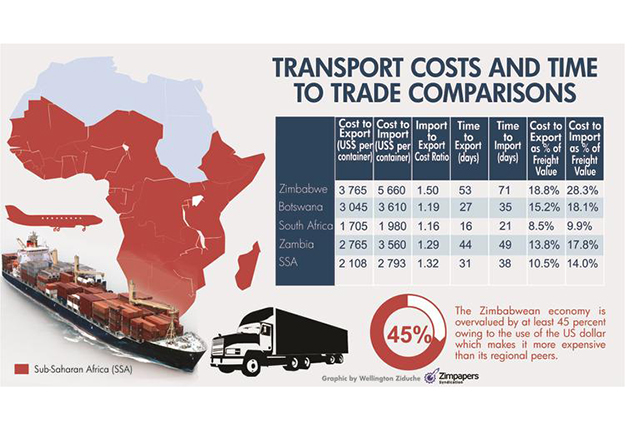

The Zimbabwean economy is overvalued by at least 45 percent owing to the use of the US dollar which makes it more expensive than its regional peers.

Speaking at the Zimbabwe economic review and national competitiveness conference recently,

Reserve Bank of Zimbabwe deputy governor Dr Khuphukile Mlambo said the high cost of finance has made it difficult for local manufacturers to penetrate the domestic market let alone compete with imports.

On average, Zimbabwean lenders charge as much as 11,4 percent on short term loans, second only to Zambia in the Sadc region. Zambia charges 11,5 percent.

Lending rates range between 4 percent and 10,5 percent in Mauritius, Botswana, South Africa, and Kenya.

Dr Mlambo said Zimbabwe’s interest rates are essentially higher than Zambia given the use of the stronger US dollar.

“Let’s remember that although Zambia’s (interest rates) may be higher, (but) it may not be that high because we are talking about cost of funds on USD for Zimbabwe and Zambia is talking of kwacha.

“So the cost of funds on a dollar elsewhere is around less than 5 percent and we are at 11 percent. In real terms it means the cost of fund is much higher here,” he said.

Dr Mlambo reiterated the importance of financial institutions in enhancing the competitiveness of local industry.

However, financial institutions’ support for local industry has been limited due to lack of liquidity, limited access to lines of credit and the strong USD against trading partner currencies especially the South African rand.

The sector has also been hounded by lack of long term deposits coupled with a high non-performing loan ratio.

“Banks and other financial institutions help solve problems of adverse selection and moral hazard, thus reducing the cost of finance.

“Finance plays a critical role in development; it intermediates between savings and investments,” he said.

On its own part, the central bank has come up with several measures to promote industry competitiveness and ease of doing business.

The RBZ reduced lending rates from above 35 percent to between 15 percent and 18 percent and established the Zimbabwe Asset Management Company to take the burden of bad debts.

In addition to that, the RBZ also resuscitated the inter-bank market to allow an increase in circulation of credit at lower margins and introduced a 5 percent export incentive that will come in the form of the much-talked bond notes.

The export incentive is really a good initiative that could see the country reducing its trade deficit through increased exports.

However, this can only happen if export and import costs are aligned with the region.

As it stands, Zimbabwean exporters are at a disadvantage as they are paying for their products to enter or leave the country while their regional peers are paying less for the same service.

Figures from the RBZ show that Zimbabwean exporters pay $3 765 per container while those in South Africa pay almost half of that at $1 705 and those in Zambia pay $2 108 per container.

Currently, most local producers are importing raw materials to use in their industries.

But most are discouraged by the exorbitant costs they incur when they want to bring in raw materials.

Zimbabwe is way above the average cost of importing in the Sub Saharan region of $2 793 per container as it costs $5 660 per container while South African importers only pay $1 980 per container. Botswana and Zambian importers pay $3 610 and $3 560 per container.

It also takes less time to export or import in Botswana, Zambia and South Africa than it does in Zimbabwe.

All this then contributes to the high landing costs of Zimbabwean products which has made them uncompetitive compared to those from the region.

Also contributing to the country’s lack of competitiveness is the limited source of revenue for Government.

Analysts believe that if Zimbabwe expands its revenue income streams, it will promote a more conducive operating environment for local producers.

The country runs on a cash budget financed almost entirely by taxes, which have become a huge drain on companies and individuals.

Dr Mlambo says the country’s tax rate as a share of GDP is between 26 and 28 percent and it is almost impossible to expect to get more from taxes from a people that are already paying this much.

But revenue from taxes has been shrinking along with the formal economy. Corporate tax, which was a major source of revenue in the past, has significantly declined to $144 million in the half year to June from $167 million in the same period last year.

Revenue realised from Pay-As-You-Earn has also slipped as most companies seek to downsize their workforce to cut costs or shut down operations.

“As industries are closing there is less and less corporate tax and less workers who contribute tax as we informalise,” Dr Mlambo said.

It is therefore imperative to improve competitiveness on all subsectors of the economy. Now, more than ever, there is need for increased push for value addition and beneficiation of the country’s produce.

This includes the minerals that are being exported raw or semi-processed and the agricultural produce ranging from tobacco, cotton, soya beans, maize and nuts that are also not utilising the value chain.

Dr Mlambo said providing finance to the whole value chain could be a way to make sure that local produce is beneficiated and benefits local companies and individuals.

“Value chain financing helps the chains become more inclusive, by making resources available for smallholders or SMEs to integrate into higher value markets,” he noted.

Above all, he said, collaborative effort is required to deal with the key competitiveness challenges in the country. —Zimpapers Syndication.